2022 – Inflation and the Impact of Transfer Pricing for your Business

Introduction

In addition to the festivities so often associated with this time of year, December is also a time to reflect on the preceding 12 months and consider what the New Year may bring.

When we reflect on 2022, one of the defining features has been the marked increase in inflation across the globe. We have seen inflation impact all major economies in 2022, with key markets such as Europe, the United Kingdom and the United States recording their highest inflation rates in decades. Some of the key drivers have been the disruption in global supply chains of both food and energy due to the ongoing conflict in Europe, as well as the over stimulation of developed economies as a result of quantitative easing and other stimulus measures employed by governments to counteract the impact of the pandemic on global markets.

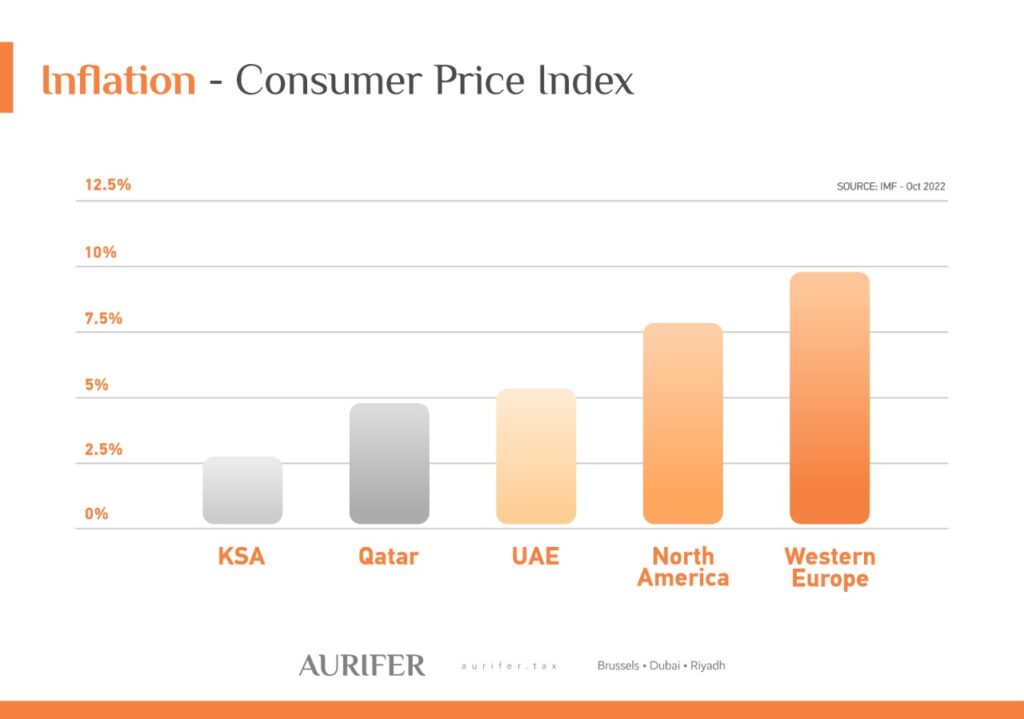

Due in part to the Gulf Cooperation Council’s (GCC) status as one of the world’s primary energy exporters, the impact of inflation has been relatively less severe than in other parts of the world. However, the GCC nations have not been immune to the rise in inflation. As of October 2022, the International Monetary Fund (IMF) reported the United Arab Emirates’ (UAE) average Consumer Price Inflation (CPI) rate was 5.2%, up from 0.2% in 2021. Similarly, Qatar’s CPI rate has increased considerably from 2.3% to 4.5% in the same timeframe.

Impact of Inflation

In a business context, the impact of inflation has been significant for both Small and Medium Enterprises (SME) and multinationals globally. Increased supply chain costs have put negative pressure on business margins and the rise in interest rates, employed as an effort to curb inflation, have impacted companies’ ability to obtain debt financing and subsequently affected cash flow and liquidity.

Transfer pricing is predicated on the Arm’s Length Principle (ALP), which states that the commercial and financial arrangements between related parties are conducted in a manner that is consistent with arrangements between independent enterprises. In this regard, the abovementioned economic circumstances have had a profound affect on pricing arrangements between independent enterprises globally.

As such, it is important for multinationals to consider the impact of inflation on their existing transfer pricing arrangements and operating model, to determine whether an adjustment is required on a go-forward basis. For businesses operating in the UAE, where the introduction of formal transfer pricing rules is imminent, it will also be important to appropriately factor these changes in economic circumstances into any prospective transfer pricing policy/operating model.

Given the pervasive impact transfer pricing can have on a multinational’s tax arrangements (taxable profit, Value Added Tax (VAT), customs duties etc.), it is important to be proactive in addressing these considerations for your business and appropriately factoring it into the 2023 planning cycle.

Mechanical Impact

As outlined above, inflation can have a significant financial impact on businesses. The relative impact of inflation on the mechanical operation of a group’s transfer pricing policy is dependent on the nature of the intercompany arrangements, as well as the transfer pricing methodology applied.

For example, a Limited Risk Distribution (LRD) entity that is remunerated with a fixed operating margin (operating profit/revenue) may require a manual transfer pricing adjustment at year-end to account for inflation, to ensure that the LRD’s margin remains aligned with the transfer pricing policy.

In contrast, where an entity performs contract manufacturing and is remunerated with a mark-up on its cost, any increase in the underlying cost base as a result of inflation should automatically be reflected in the contract manufacturer’s return, as the basis of remuneration (i.e., cost) correlates with the impact of inflation.

However, although a cost-plus return may not be disrupted from the perspective of the contract manufacturer, the higher cost base will impact the profit margin of the counterparty compared to forecasts. Below, we discuss the impact of inflation on the group and how to effectively manage these negative impacts.

Allocation of Risk, Reward and Downside Impact

Under the arm’s length principle, the attribution of business profit amongst group entities should be aligned with each entity’s relative contribution to the functions, assets, and risks of the business.

In this regard, group entities that perform high-value functions and/or assume, control, and have the financial capacity to bear the key market and other operational risks are rewarded with an entrepreneurial return. An entrepreneurial return is typically the residual system profit after rewarding related parties that perform routine activities with a fixed return (“routine returns”).

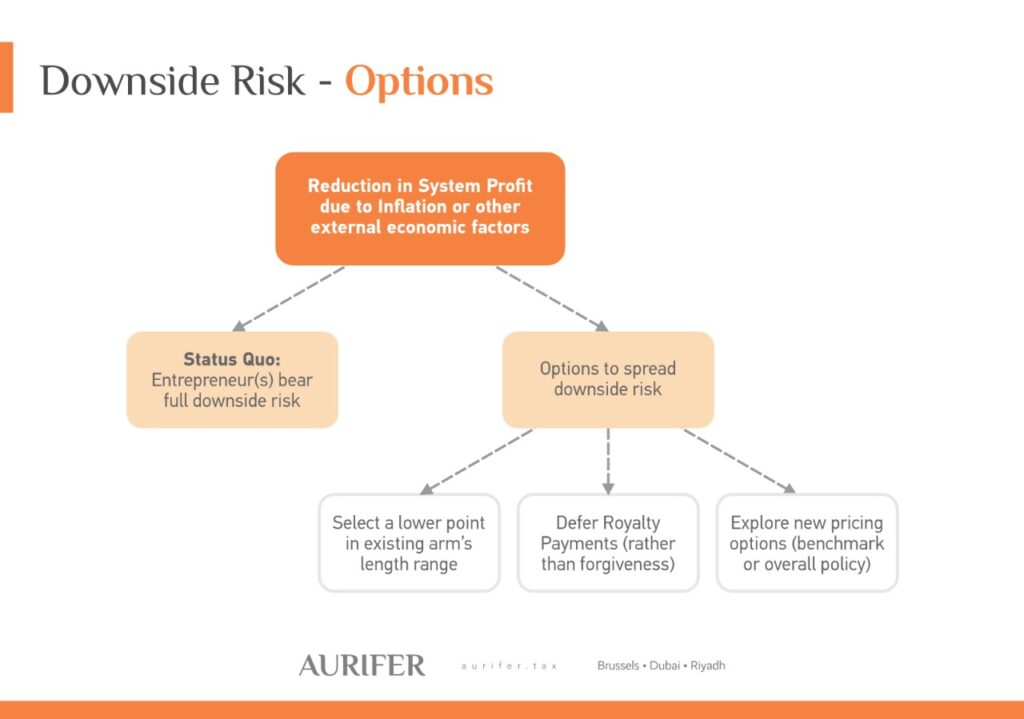

Under both examples discussed above, we considered how transfer pricing policies adapt to the impact of inflation from the perspective of maintaining the remuneration profile of the routine return entities. However, where the system profit is substantially reduced as a result of inflation or wider economic downturn, the question arises whether the existing remuneration policy remains fit for purpose and appropriately rewards each entity for its relative contribution to the group’s activities.

Under first principles, an entrepreneurial entity that retains any upside on the residual system profit should equally bear the downside risk associated with inflation/economic downturn on group profit. However, as often is the case in transfer pricing, nothing is ever so black and white.

For example, there may be commercial, regulatory, or capital requirements that could impact the entrepreneur (and the business as a whole) which would necessitate an adjustment to the group’s pricing policies to reflect market conditions. In these circumstances, an independent enterprise acting at arm’s length would be expected to re-negotiate existing arrangements to protect themselves from such consequences.

In this regard, there are a number of methods that could be employed to effectively spread downside risk amongst related parties while maintaining the arm’s length principle:

- Selection of a lower point in the arm’s length range. The selection of a point within the interquartile range may be appropriate. An adjustment should be applied in accordance with the terms of the intercompany agreement and supported by robust documentation outlining the rationale for the adjustment, as it is likely to be challenged from the local tax authority of the routine entity.

- Defer payments until a recovery in economic circumstances. This situation may be more relevant for royalty license arrangements. Rather than a complete forgiveness of a royalty payment, a licensor may allow licensees to defer payment until such time as the economic circumstances have improved. Again, consideration to the terms of the existing intercompany agreement and appropriate support documentation is required. It may be appropriate for the licensor to apply a small portion of interest, as the characterization of the arrangement may take the form of a loan or working capital balance.

- New transfer pricing policy/benchmarking. Performance of an updated benchmarking or implementation of a new operating model may result in a more equitable distribution of profits/losses between group entities.

The appropriateness of the above options will depend on each business’s specific facts and circumstances, the risks for which each entity is responsible, the impact of inflation on system profit etc. We would advise that these points are considered and addressed pro-actively, as retrospective adjustments may be more likely to be challenged by tax authorities.

Finance Arrangements

As indicated above, one of the key measures adopted by central banks to counteract inflation has been to increase interest rates. These measures have had a seismic effect on capital markets and the liquidity of multinationals and SMEs.

From a transfer pricing perspective, where the group’s external borrowing costs have increased significantly as a result of these measures, this should be appropriately reflected in prospective intercompany loans. It may be possible to reflect this change in economic circumstances through application of an increased rate of interest or the introduction of additional loan fees and charges (e.g., commitment fees, annual fees etc.) to ensure the lender is appropriately rewarded. In this regard, multinationals should ensure that their interest rate benchmarking analyses are up to date such that the group’s financing arrangements are reflective of the financial markets at the time a loan is entered into.

Inflation and higher interest rates may also affect a borrower’s key financial metrics. In the context of debt financing, this could impact the borrower’s credit rating and/or ability to demonstrate that the quantum of intercompany debt it has on its balance sheet is not excessive relative to ordinary market behavior. This in turn may impact the group’s ability to claim interest deductions on its existing or prospective debt. An assessment of these metrics is an important step to consider when determining the debt/equity mix for companies in 2023.

Separate to intercompany financing, rising interest rates may also affect the valuation of intellectual property and other assets when priced using an income-based approach. The underlying premise of this approach is that the value of an asset can be measured by the net present value of the economic benefit to be received over the life of the asset. The steps followed in applying this approach include estimating the expected cash flows attributable to an asset over its life and converting these cash flows to a net present value using an appropriate discount rate.

In principle, an increase in the cost of debt would lead to an overall increase in the discount rate applied. Ultimately, a higher discount rate would reduce the net present value (i.e., price) of the asset.

Documentation

Finally, multinationals should be considerate of the impact of inflation and other economic shocks from a documentation and benchmarking perspective.

For example, many jurisdictions allow companies to maintain a TNMM benchmarking for up to three years (with an annual financial refresh), before a full re-performance is required. This is based on the recommendation in the OECD Guidelines on the frequency of documentation updates. However, the key caveat for this allowance is that there is no change to the operating conditions, including economic circumstances, to the controlled transaction. Any of the abovementioned factors discussed may trigger the requirement to re-perform an existing benchmarking analysis.

Additionally, we note that many jurisdictions in the GCC have a strong preference for the use of local comparables (e.g., Saudi Arabia). However, in practice it is common for a benchmarking analysis to incorporate comparables from other jurisdictions, including Africa and Eastern Europe, in an arm’s length range.

The OECD Guidelines indicate that arm’s length prices may vary across different markets even for transactions involving the same property or services. As such, in order to achieve comparability, the markets in which the independent and associated enterprises operate should not have differences that have a material effect on price. In this regard, given the relative impact of inflation and other economic and political circumstances in places such as Eastern Europe compared to the GCC, these practices may no longer be appropriate over the short-term.

However, the OECD Guidelines suggest that it may still be appropriate to rely on such comparables where appropriate adjustments can be made. Where it is not possible to completely eliminate these jurisdictions from a comparable set, appropriate adjustments to reflect the difference in inflation or other economic differences should be reflected in the transfer pricing documentation.

With the forthcoming introduction of transfer pricing in the UAE, transfer pricing continues to gain momentum in the GCC. As such, multinationals should be pro-active in determining an appropriate operating model and transfer pricing policy for the region. As part of this, companies need to make sure they consider the wider global economic circumstances in addition to their specific business strategies and plan accordingly.