Explore the complexities of real estate investment taxation in the UAE with the article “Immovable Property Income in the UAE: Tax Implications for Domestic and Foreign Investors.”

This piece, authored by our very own Thomas Vanhee, Priyanka Naik, and Giorgio Beretta, and featured in Tax Notes International on December 18, 2023, offers a detailed look at the new corporate tax landscape effective June 1, 2023.

It provides valuable insights for both local and international investors navigating the UAE’s real estate market.

Click to read the full article and stay informed about these essential tax developments.

Our business survey shows how ready businesses are about the OECD/G20’s Pillar Two Initiative.

Aurifer Middle East had the privilege of representing the business community at the UNCTAD’s 8th World Investment Forum held in Abu Dhabi, a reason it conducted a survey for MNE’s operating in the UAE and the Gulf to gauge where businesses stand and their readiness to adapt to the impending changes of the OECD/G20’s Pillar Two Initiative. The data and sentiments captured in this survey were shared in the forum, bringing the GCC business perspective to a global stage.

Read our survey.

The United Arab Emirates (UAE) introduced the Economic Substance Regulations (ESR) in April 2019 to be excluded from the EU’s COCG grey list (European Union’s Code of Conduct Group) and not to be classified as a harmful tax jurisdiction by the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS).

Not long after its introduction, UAE launched a new (amended) ESR legislation in August 2020, which was based on the outcome of the review of the no or only nominal tax (NOON) jurisdictions, concluded in June 2019, by the OECD’s Forum on Harmful Tax Practices (FHTP). The new law is more aligned to the international standards stipulated in the BEPS Action 5 and is retroactively effective from 1 January 2019.

The new ESR law introduced exciting amendments, such as: granting exemptions to branches and permanent establishments of foreign entities from meeting the substance test, expanding the scope of the distribution and service centre business, extending its applicability to government entities having a global presence, etc. In addition to this, the new ESR legislation granted substantial powers to the Federal Tax Authority (FTA) to oversee compliance, perform assessments and impose administrative penalties on defaulters.

The Ministry of Finance (MoF) also built a dedicated portal for licensees to submit their ESR notifications and reports to encourage compliance. Through this portal, licensees remain up to date about their ESR obligations, receive enquiries and assessment and penalty notices from the Regulatory Authorities (RA) or the FTA through the same channel.

In response to the ESR submissions made by the licensees for FY 2019, the RA and FTA have been reasonably active in asking for explanations and documentary pieces of evidence to substantiate the exemption status or meeting the economic substance test. In certain cases, the Regulatory Authorities have requested licensees to provide their land lease agreements, minutes of board meetings, outsourcing agreements, and other documentary evidence to prove that it meets the economic substance test. In other cases, the request for information was vague and broad, leaving room for a lot of interpretation. It is also observed that the RA/FTA have not hesitated to levy penalties in cases where the licensees have failed to comply with the ESR obligations.

To resolve technical errors, the support team at the Ministry of Finance (MoF) has been responsive over emails and calls. Additionally, licensees are allowed to rectify/amend the submitted ESR notifications or reports without levying additional penalties (although the deadline may be very short, e.g., five (5) business days).

Despite the available guidance and technical support from the MoF, licensees faced several challenges in meeting the ESR requirements, e.g., identifying the ultimate parent entity and/or ultimate beneficial owners in limited liability partnership structures, calculating the income/expense related to the relevant activities in the absence of prescribed methods, classification of the relevant activities, meeting the branch exemption, etc. Licensees also struggled to meet the substance test that requires them to substantiate the fact that they carry out the relevant activity, i.e., they are directed and managed in the UAE, and they meet the “adequacy test”, i.e., they have adequate expenditure, premises and employees to conduct their business operations in the UAE, either themselves or through an outsourcing service provider.

With several factors involved in doing business globally, Multinational Enterprises (MNE’s) might fail to meet the substance test in the UAE. Failure in meeting the substance test results in an administrative penalty of AED 50,000 for the first offence and AED 400,000 for a subsequent one. Further, it may also result in other countries taking defensive measures such as denying deductions, imposing withholding taxes on payments to companies or applying controlled foreign corporation rules to subsidiaries in such jurisdictions.

The key takeaway from this discussion is:

The implementation of ESR by the UAE is subject to a peer review from January 2021 to ensure the standard is effectively implemented by UAE. As a result, UAE may amend its ESR legislation in the future again.

Round 1 of the ESR was underestimated by the businesses, but the RA/FTA took it seriously. Therefore, as a forewarning for round 2, businesses that carry out one or more relevant activity in the UAE must either consider increasing their substance if not adequate or consider alternative restructuring options, e.g., redomiciliation into another jurisdiction, restructuring, liquidation, etc., to dodge the substance requirements. Tax payers who fail to meet the substance test for a second consecutive year will be exposed to a penalty of AED 400,000, and, what is probably worse, the tax authority of the parent jurisdiction will be informed of the lack of substance in the UAE.

Our previously conducted webinar may help in filling out the notifications and forms. Additionally, consistency in meeting the different disclosure requirements is important, as Ultimate Beneficial Owner filings and the Country by Country reporting may require similar information to be disclosed and these disclosures allow reconciliation with the ESR information disclosed.

Round 2 starts with notifications by end of June 2021 for FY 2020. Tax payers have been warned.

With increasing globalization and the ease of conducting international financial transactions, the G20 countries requested the OECD to develop a transparent system that would allow jurisdictions to combat off-shore tax evasion and non-compliance effectively. Although exchange of information was not a foreign concept, CRS is one example of an international evolution towards automatic exchange of information (AEOI) based on pre-defined formats. Another such an example is country by country reporting.

Drawing inspiration from the Foreign Account Tax Compliance Act (FATCA) in the USA, the OECD Council approved the Common Reporting Standards (“CRS”) in 2014, enabling the automatic exchange of financial information between jurisdictions.

How does it work?

A Financial Institution (e.g. a bank) in jurisdiction A collects select information and reports it to its local competent authority. Based on this information, the local competent authority of jurisdiction A will exchange the account information of persons who are tax resident in a different jurisdiction (e.g. jurisdiction B). This information will be exchanged directly with the competent authority of the jurisdiction B on an annual basis and it will include the following information:

Upon the receipt of the above information, the tax authority of the jurisdiction B will determine whether the taxpayer discloses his income accurately and if sufficient tax is paid. This process ensures that the taxpayer fairly discloses his income in jurisdiction B and jurisdiction B rightfully receives tax that is due from the taxpayer.

Legal instruments

A country implementing CRS adopts certain legal instruments. It includes the Multilateral Competent Authority Agreement on Automatic Exchange of Financial Information (“MCAA”) and the Multilateral Convention on Mutual Administrative Assistance in Tax Matters (“MAC”).

The MCAA includes the rules of exchange of information between foreign jurisdictions and also provides the infrastructure to safeguard confidential information being exchanged. As on 25 November 2020, 105 countries are signatories of the MCAA with the first exchange of information having started in September 2017.

CRS in the UAE

The UAE has opted for the widest approach for CRS and the UAE Ministry of Finance (“UAE MoF”) acts as the Competent Authority in charge of CRS implementation and ultimately enables the exchange of information with foreign jurisdictions. Moreover, it has ratified both the MCAA and MAC in 2018.

The UAE has appointed multiple Regulatory Authorities for implementing CRS in the UAE, these authorities are:

With the recent merger of the Insurance Authority with the UAE Central bank, the UAE may have at least five sets of Regulations for CRS purposes.

The first exchange of information between the UAE MoF and the participating reportable jurisdictions with UAE has taken place on 30 September 2018. The USA is excluded from the CRS as, as mentioned above, it adopted its own set of legislation.

Impact on Financial Institutions

Financial institutions hold a fundamental role in the effective implementation of CRS in the country. They are intermediaries through which the regulatory authorities collect information required for exchange of information purposes.

Reportable Financial Institutions include Custodial, Depository, Investment and Insurance Institutions.

In order to determine whether a pre-existing or new account is a Reportable Account, the Financial Institutions are required to put due diligence measures in place and collect relevant information from their clients (e.g. tax residency, TIN). These due diligence measures can be incorporated into existing AML measures, KYC policies, or by obtaining and validating self-certifications from account holders.

If an Account holder is a Passive Non-Financial Entities (“Passive NFE”), the Financial Institution must also identify the identity of the natural person(s) who exercise control of the legal person via a controlling ownership. The Financial Action Task Force (‘FATF’) recommendation determines that controlling ownership interest can be based on a threshold, for example, a natural person owning more than 25% of the legal entity would be identified as the Controlling Person. If no person can be determined through ownership, Financial Institutions must also determine if a person exerts control over the legal entity through other means.

Another aspect that Financial Institutions have to consider is OECD’s analysis of high-risk CBI/RBI schemes when completing due diligence procedures. Citizen by Investment (‘CBI’) or Resident by Investment (‘RBI’) schemes allow individuals to obtain citizenship or resident status by making local investments. The OECD has established a list of countries that offer such schemes which includes the UAE and Bahrain.

Additionally, financial institutions are required to submit an annual report (by 30th June in the UAE) to their regulatory authorities describing the due diligence procedures in place, the number of reportable accounts, the amounts within these accounts (in USD), and other information.

Due to their important roles in the information collection processes, Financial Institutions may incur heavy compliance costs and spend more time on validation and reporting.

The UAE Cabinet recently published Cabinet Resolution No. 5/11 of 2020 Session No. (11) which imposes a penalty of AED 1,000 on any financial institution that opens a new account without obtaining a valid self-certification or for failing to validate such self-certification.

In recent times, the UAE has taken a stricter approach towards compliance, on the one hand reinforcing the penalty framework, and on the other hand enforcing stricter compliance on financial institutions.

Impact on account holders

New and/or pre-existing account holders are requested to provide a self-certification which contains information of the individual’s name, place of birth and jurisdictions the customer is tax resident.

Entities have to provide a more comprehensive self-certification form with special emphasis on entities that are Passive NFEs (which helps identify Controlling Persons).

It is crucial for individuals to determine and inform their tax residency in the self-declaration form as in principle, the financial institutions are not permitted to assist the individual in this process.

The UAE has recently expanded the definition for being a tax residence in the UAE. In case of new individuals accounts, documentary evidence of a valid UAE residence visa must be available.

Enhanced Due Diligence procedures will be carried out by the respective Financial Institution for account holders with a valid residency visa of more than 5 years and if the Financial Institution cannot validate the self-certification provided by this individual.

To discourage account holders from providing inaccurate or insufficient self-certifications, a fine amounting to AED 20,000 may be imposed on the account holder (or the controlling person).

Pitfalls

Despite the clear Common Reporting Standards, certain structures may still lead to non reporting of financial accounts. In addition, the tax residency criteria may differ from one jurisdiction to another, and unlike for international tax, there are no treaties providing tie breaker rules. This means amongst others that persons can have dual residences, and that for example a person who has acquired residency (or citizenship) by investment could be considered as a resident in the country of investment, whereas he is actually a tax resident in another country.

The UAE however, has recently updated its tax residency definition to to take into account these RBI/CBI schemes.

Despite the rules becoming stricter and the enforcement more intense, there are still a number of service providers which propose structures to avoid CRS reporting which will ultimately not reach their goal.

Ultimately, much confidence is placed in the due diligence process with the banks. Compliance is not always straightforward for financial institutions, who depend on the information disclosed to them and might not have much additional information to compare with. Amending submitted reports is also not an easy process.

Errors in CRS reporting may lead to incorrect exchange of information and affect account holders in the long run. A convenient and lenient correction process can encourage Financial Institutions to disclose errors without the fear of facing penalties.

Ultimately, the stricter enforcement of CRS is another step towards transparency taken by the UAE and individuals and businesses need to analyze their structures from this point of view, even more so today than when CRS was introduced in the UAE.

Now that the UAE MoF has opened the portal, let’s have a look at how we can file the ESR notification and report.

If you have missed our webinar, no worries, you can find it back by clicking here.

Do not miss our webinar covering the year 2020 in review from a GCC tax perspective.

Attend our webinar on 18 January and make sure you are up to date with every single tax development in the GCC.

Are you afraid you missed the KSA guides and Circulars? That you missed the Clarifications in the UAE? Did you miss the Omani TP updates? Did you not review the changes in the KSA income tax law?

We will cover all important 2020 updates across the GCC and across all taxes. We will also cover our expectations in terms of the 2021 changes.

The webinar is a must attend for any in-house tax person.

Registration via lovely@aurifer.tax. Seats are limited!

By way of Cabinet Decision No. 58 of 2020, the UAE has implemented a new UBO regime applicable to businesses established in the UAE, except for ADGM and DIFC businesses. The latter are subject to their own regulations. Government owned businesses are also excluded.

Under the new UBO regime, businesses in the UAE are subject to more strict compliance obligations. For some Free Zones, certain requirements were already in place, and therefore the new regime does not change much.

The new UBO regime stems from the Anti Money Laundering legislation in the UAE, more in particular Federal Decree-Law No. 20/2018 and its Implementing Regulation. It is suspected to target amongst others disclosures of nominee structures.

The new UBO regime requires businesses in the UAE to maintain beneficial ownership and shareholder registers at their registered office, and to submit information from these registers to their regulatory authority (e.g. DED or Free Zone Authority). Any changes in the information previously provided, need to be disclosed as well.

Keeping a UBO Register

The requirement to submit the UBO Register has been in place before and was sometimes required e.g. upon issuance of the trade license of a new entity in the UAE. However, with the latest Decision, UAE entities are required to maintain a UBO Register and update the Regulators accordingly for any changes.

Who is the UBO?

A beneficial owner can be determined as follows:

What goes in the UBO Register

The UBO Register needs to contain the following information on the UBO:

Shareholder or Partner Register

Businesses are further required to hold a Shareholder or Partners Register. Holding a Shareholder or Partners Register constitutes good practice anyways, and is part of good governance for any company. That Shareholder or Partner Register will now need to be submitted as well. Changes to the Register are to be notified within 15 days as well of being aware of a change in the Register.

The Shareholder Register needs to contain:

Compliance before due date

The identification of the UBO can be quite challenging for some UAE companies which are part of a wider and more complex group, when the requirement is to identify the physical person who ultimately owns the company.

According to the new regime, the data needs to be submitted within 60 days of the date of Publication of the Decision. This needs to therefore happen on or before approximately 27 October 2020.

In conversations with the Authorities which need to receive the information, we understand however that the Authorities which need to receive the information, are not yet ready to do so.

Even though the penalty framework is not known yet, we can expect it to be strict and punitive.

Tax perspective

The recent introduction of different laws in the UAE such as the Economic Substance Regulations (ESR), Country-by-Country Reporting (CBCR) and Common Reporting Standards (CRS) also require UAE businesses to provide a certain level of information regarding the UBO. From a tax perspective, it should be ensured that the information provided to the relevant Regulatory Authorities is consistent and under no circumstances incorrect. Incorrect or misleading information may lead to significant penalties being imposed by the Authorities.

The penalty for providing inaccurate/incomplete information under different laws are:

The information will be further exchanged with other jurisdictions.

Our assistance

Should your company require assistance with the UBO compliance, Aurifer can assist you with the following:

Attend our webinar on the new ESR law in the UAE. Register via lovely@aurifer.tax

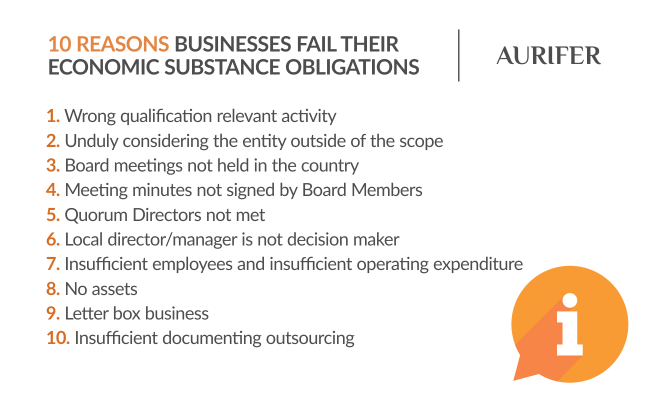

10 common reasons why businesses fail the Economic Substance Regulations Obligations

Bahrain and the UAE introduced a legal framework requiring businesses to have substance in their jurisdictions as a direct consequence of the Organisation for Economic Co-operation and Development’s (“OECD”) ongoing efforts to combat harmful tax practices under Action 5 of the Base Erosion and Profit Shifting (“BEPS”) project.

Since a number of years, the European Union publishes a list that focused on jurisdictions which may potentially be harmful to the fiscal interests of the Member States of the European Union (“EU Blacklist”). This blacklist included countries like the Bahamas, Bermuda, the British Virgin Islands (BVI), Cayman Islands, Guernsey, Isle of Man, Jersey and the UAE. In an attempt to see itself removed from the EU Blacklist, the UAE introduced Economic Substance Regulations (“ESR”) with effect from 30 April 2019. In the same year, Bahrain also introduced ESR Requirements with the same purpose.

Accordingly, Bahraini businesses and UAE onshore and free zone entities that carry on specific activities mentioned in the regulations will need to examine whether they meet the economic substance requirements. These specific activities are either highly mobile activities (e.g. licensing intellectual property, services centers, holdings, …) or tightly regulated activities (e.g. banking, insurance, …).

Businesses in scope of the ESR in the UAE must meet the Economic Substance Test. The test includes the following:

With ESR reports for the non financial sector in Bahrain for 2019 just submitted end of June 2020 and around five months left for the submission of the first ESR reports to the respective Regulatory Authorities in the UAE, we have highlighted the top 10 reason businesses fail to meet their obligations under the ESR in the UAE and in Bahrain.

1. Wrong qualification relevant activity

The relevant activities in the scope of ESR can sometimes be tricky to analyze. For example, if a company undertakes a headquarters business in the UAE, the definition of the relevant activity includes providing ‘senior management services to one of more foreign connected persons’. There is not a great deal of detail known on how to interpret this criterion and it may be complicated to assess.

Similarly, such a business may also qualify as a distribution and service centre business as it provides ‘services to foreign connected persons in connection with a business outside UAE’ (i.e. a foreign subsidiary). The definition of a service centre business in the UAE is extremely wide and catches many more businesses than one would expect.

In such cases, the Relevant Activities guide and the FAQs published by the Ministry of Finance is helpful to determine whether the licensee falls within the scope of both the relevant activities and based on which relevant activity must the ESR test be fulfilled and must be reported. In this case the licensee will have to meet the ESR test only for the headquarters business and not the distribution and service centre business. However, it is still unclear how this will be conveyed in the ESR report.

Another example relates to intra group financing. Although these businesses provide financing and fall inside the scope of ESR, they may encounter practical difficulties of identifying their appropriate relevant activity and regulatory authorities.

2. Unduly considering entity outside of the scope

Licensees in the region sometimes assume that, since their trade license does not mention any of the relevant activities, the entity is outside the scope of ESR. The ESR regulations however adopt a ‘substance over form’ approach. Therefore, irrespective of the activities mentioned in the trade licence, if any licensee carries out any of the relevant activities, they are in the scope of ESR.

3. Board meetings not held in the country

It is common practice in the UAE and Bahrain that board meetings are held via conference calls as a majority of the board members may not be based in the Gulf. The number of board meetings will be dependent on the level of Relevant Activity carried out by a licensee. However, for example in the UAE, it is expected that at least one meeting is held in a financial year in the UAE.

It may also be required to meet the minimum requirement under the law applicable to the licensee or in the constitutional documents of the licensee.

4. Meeting minutes not signed by Board Members

In the UAE, it is also required that these meeting minutes are signed by the directors that are physically present at the meeting and these minutes must be kept in the UAE.

5. Quorum directors not met

If board meetings are held in the UAE it is essential to maintain the Quorum as per the law applicable to the licensee or as set out in the constitutional documents of the licensee.

This goes hand in hand with the requirement to maintain meeting minutes as the meeting minutes can prove that relevant decisions are taken in the UAE and that the required number of directors were present to meet the quorum for the board meeting.

It should be noted that, the UAE Ministry of Finance has notified that it will take the effect into consideration of the COVID-19 travel, quarantine and self-isolation restrictions while determining whether the ‘directed and managed’ criteria is met for the reporting year 2020.

6. Local director/manager is not decision maker

Sometimes directors or managers are appointed just to meet regulatory requirements and they only give effect to decisions taken outside the UAE. In this case, the ‘directed and managed in the UAE’ criteria for the Economic Substance Test will not be met.

As per the ministerial decision, the board or manager must have the necessary knowledge and expertise and ensure that they do not merely give effect to decisions that were taken outside the UAE. This criteria may not be fulfilled when there are only a limited number of directors in the UAE and if their role does not relate to the relevant activity.

7. Insufficient employees and insufficient operating expenses

According to the ESR, the licensee must demonstrate that it has an adequate and appropriate number of qualified full-time employees engaged in the relevant activity and that these employees are physically present in UAE. Similarly, sufficient operating expenses must also be incurred in the UAE depending on the level of activity in the UAE.

However, the term ‘adequate’ and ‘appropriate’ is subjective and it depends on the nature and level of the relevant activities conducted by the licensee. Additionally, the regulatory authority may have its own minimum requirement for the purposes of receiving a valid trade license. For example, it may be appropriate for a holding company business to not have any full-time employees or office premises in order to conduct this business.

8. No assets

The ESR also requires the licensee to have adequate physical assets for the relevant activity. This requirement mainly relates to procuring adequate premises to carry out a Relevant Activity in the UAE. Premises can include offices or other form of business premises depending on the nature of the Relevant Activities. Furthermore the premises may be owned or leased by the licensee.

This means that businesses with ‘flexi-desk offices’ in the UAE conducting a holding company business may meet the criteria of adequate sufficient premises. In contrast, a business that conducts a headquarters business responsible for the GCC region may at least require regular office premises in the UAE.

9. Letterbox business

The ESR is mainly aimed at such entities as they do not have sufficient substance in the UAE. These ‘letterbox’ entities are usually established in a Free Zone with minimal operating expenses and no premises. The purpose of these entities is mainly to be the middleman in different international transactions for the purposes of shifting profits and reducing the burden of taxes.

10. Insufficient documenting outsourcing

A licensee may satisfy the sufficient activities, employees, operating expenditures and/or premises criteria for the Economic Substance Test, if they are provided by a third party. These functions can be outsourced provided sufficient documentation is maintained and the activities are undertaken in the UAE.

Additionally, the licensee must be able to demonstrate its ability to supervise the carrying out of CIGA by the third party service provider (where applicable) as the licensee remains responsible for accurate reporting at all times.

It is likely that the majority of licensees may not have sufficient documentation that can be provided to the Regulatory Authorities in this respect.

Consequences of failing to meet the test

First time failures to meet the Economic Substance Test, will attract a penalty ranging from AED 10,000 to AED 50,000. Any subsequent failure will attract a penalty ranging from AED 50,000 to AED 300,000 (article 10 of the ESR).

The authority could also impose additional penalties and sanctions which may include the suspension, revocation or non-renewal of the entity’s business license.

If the Regulatory Authority determines that the licensee does not meet the Economic Substance Test and notifies the licensee of this, this information can also be exchanged with the foreign competent authority where the Ultimate Parent Entity or the Ultimate Beneficial Owner resides in or where the foreign licensee is incorporated. This may lead to tax audits or to certain tax benefits being denied.

Licensees should start early in terms of analysing whether they meet the Economic Substance Test for the year ending 2019.

Even if there is no way to remedy the past, it is better to implement the necessary measures as soon as possible. This in turn will enable the licensees to meet the Economic Substance Test for the next financial year.

Click here for Aurifer’s quick cash flow tips to increase your liquidity during these uncertain times.

JBC4 3802, Cluster N, Jumeirah Lakes Towers, Dubai, UAE.

201, 14th floor, Al Sarab Tower, ADGM Square, Abu Dhabi, U.A.E.

Al Anoud Tower L18, Office 1802 King Fahad Road Riyadh Saudi Arabia

Regus Business Centre, Floor No. 2, D Ring Road, Al Mataar, Al Qadeer District, Doha, Qatar

© Aurifer

Developed By Volga Tigris Digital Marketing Agency