KSA publishes long awaited DTT with UAE

The Double Tax Treaty (“DTT”) between the UAE and the KSA provides a significant tax incentive for businesses operating in the two contracting states. A positive impact on investment and trade between the two contracting States is expected in the aftermath of its entry into force.

This is the first DTT signed between two GCC countries. KSA is a member of the G20 and a key player in the GCC economy and on the global oil markets. It is keen to reinforce its promising investment environment. On the UAE side, the signing of this DTT reinforces its status as a regional hub for foreign investments and shows its commitment to its continued attractiveness and excellence.

Both contracting countries are members of the BEPS inclusive framework and signed the Multilateral Instrument (“MLI”). Signing such a bilateral DTT is a new step towards compliance with BEPS minimum standards – notably regarding transparency and tax avoidance. It goes hand in hand with the extensive TP legislation recently published in KSA.

This article highlights the key features of the DTT and analyses its tax implications for businesses operating in the two contracting states.

1. About the Treaty

Due to lengthy negotiations, the treaty is based on the 2014 OECD Model Tax Convention, even though the model was updated in 2017.

However, the KSA has already included this DTT in the list of its Covered Tax Agreements (“CTA”) in the MLI. It is yet to be included by the UAE, since the UAE signed the MLI shortly after the treaty.

2. Key Features

Persons covered

Only the “residents” of the contracting states shall benefit from this treaty.

This residence principle is generally adopted by the KSA in most of its recent treaties, contrary to the UAE which has recently opted for a citizenship criterion, such as for its recent DTT with Brazil.

Residence

As a primary definition for “resident”, the treaty uses the standard language of the OECD Model Tax Convention.

An additional interesting provision is that the DTT expressly qualifies as resident, any legal person established, existing and operating in accordance with the legislations of the contracting states and generally exempt from tax:

• if this exemption is for religious, educational, charity, scientific or any other similar reason; or

• if this person aims at securing pensions or similar benefits for employees.

Although the treaty does not specify whether the residence concept is applicable to businesses established in the Free Zones (UAE) or the Special Economic Zones (KSA), the competent tax authorities are required to coordinate to determine the requirements and conditions to be satisfied to be entitled to any tax benefit granted by this treaty.

Permanent Establishment “PE” Clause

The PE clause is largely based on the OECD Model Tax Convention, but features two elements inspired by the UN Model. It notably qualifies:

• As a PE: a building site, construction or installation project after 6 months (12 in the OECD Model)

• As a service PE: providing services, including consultancy services, by an enterprise through employees or other personnel engaged by the enterprise for such purpose if their presence lasts for a period or periods aggregating more than 183 days in any 12-month period

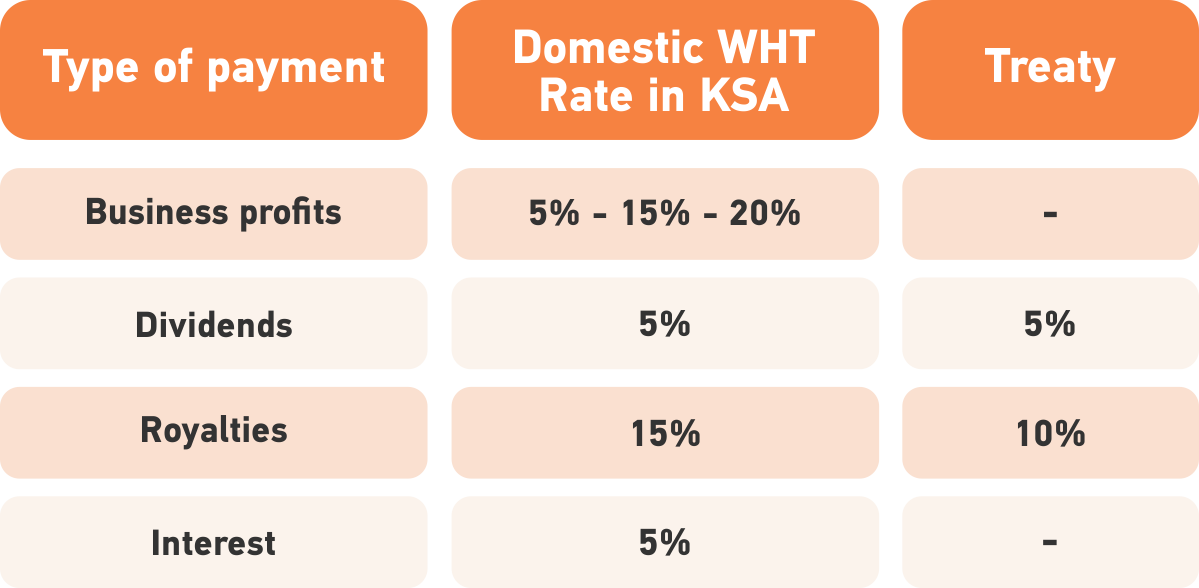

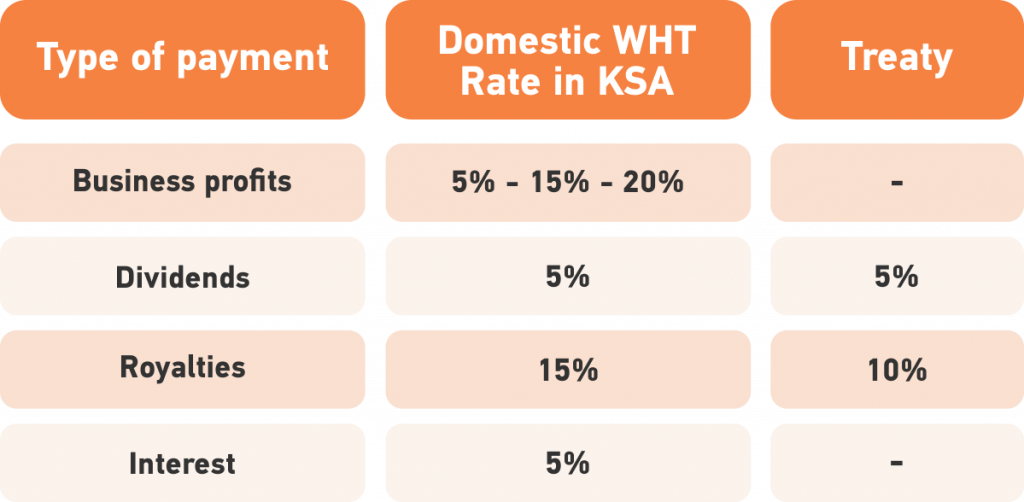

Taxes covered, rates and double taxation elimination

The DTT covers income tax and Zakat in the KSA and income tax in the UAE, inspite of the absence of a federal income tax law in the UAE.

No withholding tax regime applies in the UAE. The table added to this article shows the impact on the withholding tax rates in the KSA and the consequences of the treaty.

The DTT will not apply for royalty payments in case the beneficiary has a PE in the source country (exceptions apply). Similarly, excessive interest payments made between related parties shall not benefit from the DTT exemption.

The treaty provides for source country taxation only on income from natural resources exploration and development. The elimination of double taxation is performed through the tax credit method.

Zakat and the Treaty

Zakat is covered by the treaty (for the KSA). An interesting provision, introduced in several DTTs concluded by Saudi Arabia (e.g. Georgia, Mexico and Kazakhstan), states that “In the case of the KSA, […] the methods for elimination of double taxation will not prejudice the provisions of the Zakat collection regime.”

This provision may have an impact on Zakat for UAE businesses, considering the recent update of the Zakat implementing regulations. This notably impacts PE headquarters that might be subject to Zakat in the KSA, if specific criteria are met.

3. MAP and other provisions

The treaty provides for a Mutual Agreement Procedure (“MAP”) which can be requested to the competent authority in any of the contracting states within 3 years from the first notification of the action resulting in taxation not in accordance with the provisions of the Convention.

Investments owned by Governments (e.g. investments of Central Banks, financial authorities and governmental bodies) shall be exempt from taxes in the other contracting state. The income from such investments (including the alienation of the investment) is also exempt. The exemption does not include immovable properties or income derived from such properties.

There is no provision in the treaty for non-discrimination, assistance in the collection of taxes or territorial extension.

The entitlement to the benefits of the treaty will not be granted in case the main purpose of the transactions or the arrangements at stake is proved to be the enjoyment of such a benefit.

4. Conclusion

Even though this DTT between the KSA and the UAE is largely based on the OECD model 2014, the PE definitions it provides adopted from the UN model, broadens the scope of the activities taxable in the source countries, and will require specific attention.

The relief of withholding tax on royalties and interests, along with the MAP will reinforce the business relationships between these two countries. It is regretful that there is not a clear framework for Free Zone or Special Zone companies.

Finally, it is to be expected that the treaty will soon be notified by the UAE as a CTA under the MLI. In such case, businesses willing to benefit from this DTT will have to satisfy the Principal Purpose Test for the concerned transactions or other investment arrangements.