Over recent years, Mergers and Acquisitions (M&A) activities in the Middle East have held steady, despite the challenging economic climate across the world.

Such feat can be credited to the economic strategies implemented by the countries in the region. The United Arab Emirates (UAE) has remained the top market for M&A activity, with 155 deals worth $17.2 billion (AED 63 billion) in the first nine months of 2022, according to reports.

Saudi Arabia has also launched initiatives that had a positive impact on M&A, such as Vision 2030, the privatization of state-owned assets, and industry consolidation.

With favorable business and UAE corporate tax policies, the Middle East has become a prosperous hub for trade and investment, leading to a steady stream of M&A activity as businesses seek to access new markets and generate additional revenue streams.

In this article, we provide insights on some of the basic concepts of how to manage the tax aspects of M&A transactions. We also discuss the nuances of the law pertaining to the direct and indirect tax regime in the UAE, and how these impact M&A.

Why conduct a Tax Due Diligence?

Conducting a tax due diligence helps to assess possible tax risks associated with the target company that the buyer plans to acquire, or the seller wishes to sell.

From the buyer’s point of view, a tax due diligence is required for the following reasons:

From the seller’s point of view, a tax due diligence is required for the following reasons:

A Tax due diligence can create value. A clean slate for the target, will reduce uncertainty, and therefore increase the deal value.

Negotiating the deal and managing risk

Deals can be structured in a variety of ways, of which the simplest ones are the negotiation of outright Asset Purchase Agreements or Share Purchase Agreements.

Some of the matters that the buyer may pay attention to following a due diligence are:

Some of the matters that the seller may pay attention to are:

Often a tax ruling is highly critical in respect of the structuring of the deal itself. Having the tax authority rubberstamp the transactions helps in avoiding any future disputes.

A popular method is also to insure against the risks discussed above and to procure ‘Warranty and Indemnity Insurance’ (W&I Insurance). Essentially, W&I Insurance provides cover for losses arising from a breach of warranties and claims under tax indemnities.

This way, the benefit for the seller is that they access the sale proceeds immediately, rather than, for instance, having an amount blocked in an escrow. In turn, the buyer is protected from any unknown tax related loss, from the insurer directly, especially when the buyer is not convinced about the financial standing of the seller after closing.

From the insurer point of view, they require a thorough analysis of the tax due diligence report. This will determine any points of uncertainty, and to ensure that the scope of the insurance coverage is limited to the extent of their satisfaction, before quoting for a premium.

Read more on the importance and practice of obtaining tax insurance in the Middle East here.

Another important reason for protection against legal liabilities (during M&A transactions as well as more generally) is that sometimes, non-compliance may even trigger liability for the Directors and other executives of the company. In one of our earlier articles, we discussed the interplay with the personal liabilities of the Directors.

From Current structure (As Is) to Target structure (To Be)

Effective tax structuring is essential to mitigate the tax-related risks that can arise in M&A transactions—such as tax compliance, tax disputes, and transfer pricing. It usually involves carefully designing the structure of the transaction in a tax-efficient manner while ensuring compliance with applicable laws and regulations.

Pre-deal structuring may happen to make the Target more attractive, and Post-deal structuring may happen to align the acquisition better with the operation model of the buyer.

M&A and Direct Tax

M&A transactions have a profound accounting and valuation impact, both for the buyer and the seller. This in turn leads to a potential tax impact. For example, the M&A deal may revalue the assets and liabilities of the company, or the sale of shares may trigger a capital gain, a potential tax exposure.

Many jurisdictions have provisions under their law to reduce the impact of M&A transactions from a tax point of view, or otherwise address certain relief on certain types of reorganisations.

For example, under the UAE CIT Law, transfers of business are considered to be tax neutral and benefit from a temporary exemption of taxes, subject to conditions. This is the case where (i) businesses within the same ‘Qualifying Group’ are restructured (Article 26 UAE CIT law – we will not be covering these aspects here) or (ii) where the M&A transaction is eligible for a specific business restructuring relief (Article 27 UAE CIT Law).

The specific business restructuring relief allows sellers not to have to account for any potential capital gains (or losses) as a result of the transaction. Certain conditions need to be met, as shown below in Table 1.

Table 1 – Tax-neutral restructuring – status of parties and transfer details | |

Status of the transferor | The transferor is a taxable person |

Nature of the transfer | Transfer of entire business, (or) an independent part of the Business (as the case may be) |

Status of the transferee | The transferee is either: (a) already a Taxable Person (or) (b) will become a Taxable Person as a result of the transfer |

Consideration | In exchange of shares or other ownership interests |

Further, the conditions for availing the above benefits are as follows:

In terms of the consequences, in both situations for this benefit to accrue, the following must be observed:

The tax-neutral benefit is not available, and therefore there is a clawback, when any of the following occurs within 2 years from the date of the transfer:

If any of the above activities occur within two years, the transfer of the (independent part of the) business shall be treated as having taken place at Market Value at the date of transfer, what is popularly known as the ‘claw-back provision’.

The unutilised tax loss carry-over benefit is also subject to the transferee conducting the same or similar Business or Business Activity, following a change in ownership of more than 50%. Relevant factors to decide if the Business or Business activities conducted are same or similar include:

M&A and Indirect Tax

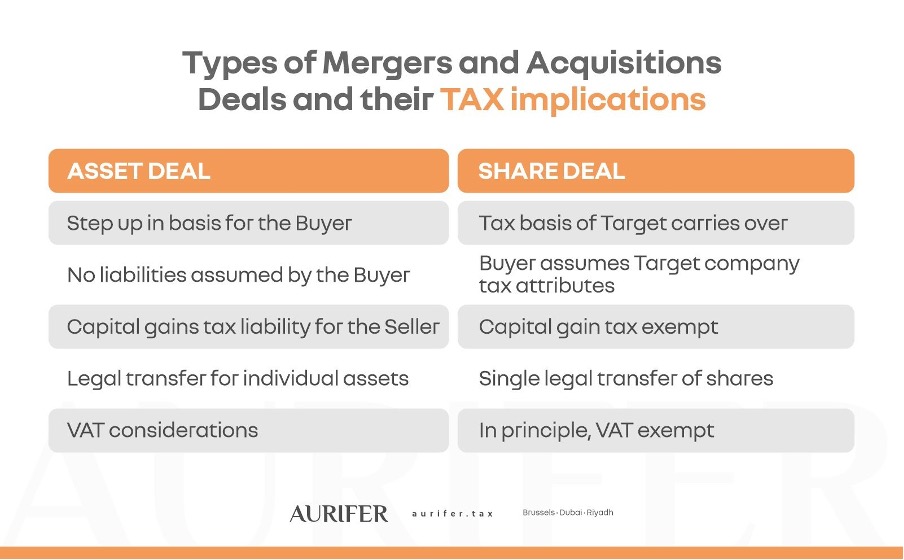

From an indirect tax point of view, it is important to note a difference between an ‘Asset Deal’ and a ‘Share Deal’.

An ‘Asset Deal’ is where the buyer acquires specific assets of the target company. The buyer does not acquire ownership of the target company itself. Instead, the target company continues to exist, and the buyer becomes the owner of the specific assets.

A ‘Share Deal’, on the other hand, is where the buyer acquires the target company by purchasing its shares. This gives the buyer full ownership and control of the target company, including all of its assets and liabilities.

Within ‘Asset deal’, there are two types of deals – (i) normal sale of assets (sale of assets) (ii) sale of assets as part of the Transfer of Going Concern (TOGC) (sale of business).

As per the clarification provided by the UAE FTA, a sale of assets is normally subject to VAT as a taxable supply. This is because only the specific assets, and not the entire business itself is transferred.

On the other hand, where the assets are sold as part of a transfer of a business as a going concern (“TOGC”), the transfer is not a ‘supply’ and no VAT is charged. For example, if the transferor sells the factory building, all the machines and transfers the rights from the employment and supply contracts, this is considered as a TOGC, and is not considered a ‘supply’ for VAT purposes. A similar understanding is given in the guidances to the Saudi Arabian VAT law, which explains the same concept referring to as a ‘Qualifying Transfer’. We have summarised the difference between an ‘Asset Deal’ and a ‘Share Deal’ in the below table:

Conclusion and Final Thoughts:

Tax advisors play a crucial role in structuring M&A deals. Over recent years, the GCC tax landscape has become increasingly complex. This is the result of a number of contributing factors, such as the introduction of VAT, frequent changes in local legislation, the implementation of the Base Erosion and Profit Shifting (BEPS) standards, increased transparency and disclosure measures (Ultimate Beneficial Ownership (UBO) reporting requirement, Common Reporting Standards / Foreign Account Tax Compliance Act (CRS/FATCA) standards, and a range of other changes.

In addition, taxpayers may have noticed an increased focus on enforcement by the tax authorities, which is evidenced by an uptake in tax audits and disputes.

We have tackled how new tax rules impact M&A deals before in one of our previous webinars, noting how tax advisory plays a critical role in M&A transactions, as tax issues can have a significant impact on the success of the deal and the post-merger integration process.

The UAE Ministry of Finance has designed a carefully balanced CIT system and has tried to avoid adversely affecting M&A transactions.

Going forward, the tax department’s involvement in the transaction will be much more important, and like in other jurisdictions, tax can sometimes make or break a deal.

The UAE CIT applies as from June 2023, but the involvement of the tax teams in the M&A deals from a UAE CIT point of view, has already started. The FTA will no doubt develop an important ruling practice important for the legal certainty around M&A Transactions.