Explore the complexities of real estate investment taxation in the UAE with the article “Immovable Property Income in the UAE: Tax Implications for Domestic and Foreign Investors.”

This piece, authored by our very own Thomas Vanhee, Priyanka Naik, and Giorgio Beretta, and featured in Tax Notes International on December 18, 2023, offers a detailed look at the new corporate tax landscape effective June 1, 2023.

It provides valuable insights for both local and international investors navigating the UAE’s real estate market.

Click to read the full article and stay informed about these essential tax developments.

Our business survey shows how ready businesses are about the OECD/G20’s Pillar Two Initiative.

Aurifer Middle East had the privilege of representing the business community at the UNCTAD’s 8th World Investment Forum held in Abu Dhabi, a reason it conducted a survey for MNE’s operating in the UAE and the Gulf to gauge where businesses stand and their readiness to adapt to the impending changes of the OECD/G20’s Pillar Two Initiative. The data and sentiments captured in this survey were shared in the forum, bringing the GCC business perspective to a global stage.

Read our survey.

The UAE has been considered a tax haven for many individuals and businesses, particularly due to its favourable tax regime. Aside from imposing no tax on personal income and personal assets, it only applies a 5% VAT on goods and services, and as low as 9% corporate tax—one of the lowest rates across the world! This is the reason why numerous entrepreneurs, the wealthy or high net worth individuals are drawn to this country. The government is keen to make doing business and living or retiring here as favourable as possible.

In addition, the government also allows easier ways to get VAT refunds for various types of entities, individuals, and organizations—giving them financial relief and attracting them further to invest in and set up a home in the country.

But how exactly do their VAT schemes usually work? We have laid out for you the different types of VAT refunds that exist in the UAE to help you understand how these regimes work.

VAT Refund for Taxable Persons in the UAE

It is obligatory for taxable persons—whether a business, sole trader, or a professional carrying out any economic activity in the country—to file returns at the end of each tax period. Aside from being compliant to the laws and regulations, this also allows them to apply for VAT refund whenever they have a VAT credit. This is provided that the input tax is greater than output tax on a VAT return.

Procedures

According to the Federal Tax Authority, here are the steps to claim for VAT Refund:

VAT Refund for Business Visitors

This specific Refund Scheme helps business visitors make a claim for refund of VAT settled on the products or services purchased in or from the UAE. The period of each refund claim is 12 months (hence at the earliest after the end of each year). The minimum amount of each refund claim to be submitted will AED 2,000.

Criteria for VAT Refund

Requirements

VAT refund for Tourists

Even the tourists and visitors can enjoy the UAE’s favorable tax refund scheme. These individuals can get VAT refund for their travel purchases in the UAE, through a special device placed at their departure port (airports, seaports, or border ports). They just need to submit the required documents and they can recover VAT from 4,000 participating retail outlets across the UAE.

Criteria for VAT refund

According to the Federal Tax Authority, for a tourist to claim VAT refund on purchases he made in the UAE, he must fulfill certain conditions:

Requirements

VAT Refund for Exhibitions and Conferences

With the aim of enhancing the country’s status as a hub for Meetings, Incentives, Conferences & Exhibitions (MICE), the UAE has allowed businesses or suppliers involved in the industry of exhibitions and conferences to also claim for refund of the VAT charged to their global customers. The scheme is made to guarantee ease of doing business, and to take the burden of tax costs from international customers.

Criteria

VAT Refund for UAE Nationals on New Residences

To provide UAE Nationals monetary relief from building a new residence in the UAE, the government has introduced a refund scheme on VAT incurred on their construction costs.

Criteria

Requirements

VAT Refund on Charities in the UAE

This VAT refund scheme, amended according to the Capital Assets Scheme, allows certain charities to recover all input tax they paid on their services and supplies. These organizations often create a blend of supplies of products and services where VAT law differ, so if such goods are supplied for a charge, FTA shall deem it as a business activity.

However, tax paid for goods used for making exempt supplies (products or services where the supplier is prohibited from charging VAT), are excluded from this recovery.

Criteria

VAT Refund for Mosque construction and operation

The Federal Tax Authority (FTA) in October launched an easier mechanism for the refund of VAT incurred on building and operating mosques. The mechanism includes refunding VAT incurred on mosques on FTA’s e-Services portal, which was formed as a result of the Cabinet Decision No. (82) of 2022 in a bid to offer financial help to mosques—considered the most important place of worship for the progressive Arab nation.

Criteria for VAT refund

Requirements

We are still awaiting the release of the Corporate Income Tax Law (CIT Law) in the United Arab Emirates (UAE). Meanwhile, there have been a slew of updates and amendments in the months of October and November 2022 in the UAE on the fronts of Income Tax, Value Added Tax (VAT) and Excise Tax. We try and cover the main amendments below.

The UAE issued Cabinet Decision No. 85 of 2022 dated 2 September 2022 (Decision), laying down the criteria for being considered as a tax resident for legal and natural persons. This is the first time that the UAE has formalized tax residency criteria at the Federal level.

The Decision is applicable from 1 March 2023. A legal person is considered a tax resident in the State if any of the following are met:

It is interesting to note that though this provision does not explicitly refer to the situation where a legal person is ‘effectively managed’ for tax residency purposes, as provided in the Public Consultation Document (PCD) in Paragraph 4.4.

Further, an individual is considered a tax resident in the UAE, if any one of the following are met:

Given the supremacy of International Law, if any Double Tax Treaty (DTT) specifies any conditions for determining a person’s tax residency, the provisions of that DTT shall apply.

The FTA also published amendments to the Federal Decree-Law No. 17 of 2017 (Decree-Law) on Excise Tax, effective from 14 October 2022. A summary of the amendments is as follows:

Where any of the reasons stipulated in the Civil Transactions Law (Federal Law No. 5 of 1985) (Civil Transactions Law), or any other law replacing the Civil Transactions Law occur, the abovementioned Statute of Limitation is to be interrupted (i.e., kept in abeyance).

The FTA also published amendments to the Federal Decree-Law No. 18 of 2022 (VAT Law Amendments) where certain Provisions of Federal Decree-Law No. (8) of 2017 on Value Added Tax (VAT Law) were amended. The VAT Law Amendments are effective as from 1 January 2023.

A summary of some of the important VAT Law Amendments is as follows:

According to the Public Clarification issued by the FTA (VATP030), this means that the place of supply of goods supplied under any contract that includes periodic payments or consecutive invoices, shall be the UAE at any time under the execution of the contract.

The residency criteria for foreign principals is inspired by the legislation covering direct taxes on PEs but includes the holding of stock, which is normally an exclusion under the PE definition in article 5 of the OECD Model Tax Convention. The inclusion of these provisions is not common for VAT purposes.

The term “market value” is not an explicit reference to transfer pricing legislation.

Prior to this amendment, the valuation of deemed supplies, based on the total cost incurred by the Taxable Personto make such deemed supplies, was not overridden by Article 36, and hence there was no explicit bar from being applicable to related party transactions.

The FTA also published amendments to the Executive Regulations to the Value Added Tax VAT Law (VAT Executive Regulations Amendments), by way of Cabinet Decision No. 99 of 2022. The VAT Executive Regulations Amendments are effective as from 1 January 2023.

The major changes in the VAT Executive Regulations Amendments are:

The record keeping provisions will likely go hand in hand with amended Emirate reporting requirements.

By and large, the changes and the amendments have been issued in light of the Government’s intention to further improve the ease of doing business in the UAE and further the UAE’s reputation of an ideal jurisdiction for Multinational Enterprises (MNEs).

With the formalization of the tax residency criteria, the building blocks of the upcoming, and perhaps imminent, CIT regime have been laid down.

Certainly, one of the most significant amendments has been to the extension of the Statute of Limitation right before some of the claims become time barred. There is also a strong emphasis on measures to counter tax evasion.

Together with the relaxation of the penalties regime last year, and a more rewarding Voluntary Disclosure regime, the face of taxes has evolved since 2017. The new rules will be tested at the event of the five year anniversary of VAT and the implementation of Corporate Income Tax.

Almost 5 years down the line for VAT in the GCC – what’s next?

As we approach 31 December 2022, the UAE and KSA will be celebrating 5 years of applying VAT. A rollercoaster ride for many in the region, authorities, advisers and in house tax managers.

We wrote in 2017 about the challenges of drafting VAT legislation in the GCC before its implementation (https://aurifer.tax/news/the-challenges-of-drafting-tax-legislation-and-implementing-a-vat-in-the-gcc/?lid=482&p=21).

We pondered whether the GCC was potentially going to be far ahead of other jurisdictions because of the Electronic Services System (“ESS”) the GCC VAT Agreement was going to implement, foreseen in article 71 of the Agreement (https://aurifer.tax/news/future-of-vat-in-the-eu/?lid=482&p=22). The GCC however never implemented the ESS. It is therefore missing an important instrument to integrate all GCC members under a single comprehensive regional VAT framework.

After almost 5 years, it’s worth taking a step back and looking at what occurred.

6 countries to implement, only 4 did

The GCC consists of six countries, Saudi Arabia, the UAE, Bahrain, Oman, Kuwait and Qatar. All countries were supposed to introduce VAT in a short span of time. The UAE and KSA did so on 1 January 2018, Bahrain on 1 January 2019, and Oman on 16 April 2021. For Qatar, rumours ebb and flow on an implementation of VAT after the World Cup, but officials are tight lipped. In terms of Kuwait, a new government is not likely to put this on the table – at least, in the near future.

The intention to implement almost simultaneously was taken with the idea of avoiding arbitrage – considering the geographical proximity between the states – and potential issues with fraud.

5% was supposed to be the rate

All 4 countries kicked off with 5% VAT, as it is foreseen in the GCC VAT Agreement as well (article 25). Saudi Arabia was the first one to hike the rate to 15% on 1 July 2020. Bahrain increased to 10% on 1 January 2022.

The increases were implemented for the same reason, as the tax was implemented for in the first place, i.e. fiscal stability. The implementation came off the back of a protracted period of running deficits for many Gulf countries. There is currently a bounce back, but how long it will take is unclear, and therefore hard to predict whether it will impact fiscal policy in the short run.

Saudi Arabia, by way of its Finance Minister, had already stated in 2021 that it would consider revising the VAT rate downwards after the pandemic. If it will happen, it will happen soon.

It’s safe to say the other GCC countries could still revise the rate upwards or downwards, depending on their specific fiscal situation.

Interestingly, the increase of the VAT rate to 15% also spawned a new tax in KSA, the Real Estate Transfer Tax (“RETT”). This new tax in KSA aimed to solve the issue of unregistered sellers, and reduce the taxes on real estate sales. Since its introduction, the RETT legislation has been amended multiple times.

The GCC countries were supposed to have numerical VAT numbers, Oman didn’t follow

In the framework of the GCC, the idea was floated to have numbers as VAT numbers. Hence, the UAE has a 1 before the number, Bahrain a 2 and Saudi a 3. Oman however choose letters and put “OM” before the number.

In the EU, VAT numbers are also composed of letters and numbers. Two letters make up the first two symbols of the VAT number and refer to a country, e.g. “LU” refers to Luxembourg (see https://taxation-customs.ec.europa.eu/vat-identification-numbers_en).

Zero rates for services are perceived a complication

5 years in, the application to zero-rate VAT on exported services, i.e., services provided to recipients outside of the GCC, remains complicated for businesses to apply and inconsistent between the GCC member states.

Although the GCC VAT Agreement for place of supply purposes looks like the EU VAT directive, from the outset, each GCC member state chose different approaches towards the place of supply of services.

B2B services were not simply located in the country of the recipient, as they are in the EU since 2010, and as is recommended by the OECD in its VAT/GST Guidelines on B2B services.

Based on an interpretation of article 34(1)(c) of the GCC VAT Agreement as laying down the rule, and including a benefit test, GCC countries have embarked on a conservative and selective interpretation of the zero rate on supplies made from a GCC country to abroad.

That conservative interpretation is not necessarily mirrored when those services are received, as there is no benefit test required there.

The rule is therefore applied unequal, and as shown by both the UAE and KSA, they felt the rule required amendments to the provision itself (https://www.linkedin.com/pulse/uae-considerably-restricts-application-vat-zero-rate-services-vanhee/). Those amendments, and ensuing clarifications have not necessarily led to more clarity.

Unfortunately, Bahrain and Oman went down the same road. A too conservative view of zero rates, can put a strain on foreign investments, as it is not easy to obtain refunds for foreign businesses (as amongst others the Saudi example shows).

As a matter of fact, disputes are common among businesses in the GCC over the VAT treatment of cross-border services due to the difference in the domestic legislation between the GCC member states and in the absence of the ESS.

Divergent policy options

The GCC VAT Framework Agreement allowed for broad policy options in the education sector, health sector, real estate sector and local transport sector. In addition, for the oil & gas sector zero rates were allowed to be implemented as well, and the financial sector could benefit from a deviating regime as well. Depending on the individual requirements and policies, the GCC Member States have implemented substantially different regimes.

None of the GCC countries so far have amended those policies in the aforementioned sectors. The UAE did move from a system where the B2B sales of diamonds was taxed, to a system where it is subject to a reverse charge as from 1 June 2018.

Tax Authority approaches

So far, in the region ZATCA has shown the most grit in terms of audits, and has lengths ahead of the other countries in terms of tax audits and disputes. KSA also had the best equipped tax authority in 2018 when VAT was introduced, although it did have to go through an organizational revamp. The UAE comes second, which is remarkable for a tax authority which only kicked off in 2017. It has been very much a rules and process based organization, which has a lot of positive effects, such as tax payers feeling treated in the same way. UAE auditors now often also give the opportunity to tax payers to voluntarily disclose their liabilities before closing the audit, which is a novely approach in the region.

The Bahraini and Omani tax authority, have been taking a more relaxed approach towards audits and disputes.

Having said the above, it’s all not all ‘sticks’ with the tax authorities. We have also observed in this 5 years, how the tax authorities, especially in KSA and the UAE, played a their role to alleviate tax from being a burden to businesses and encouraging tax compliance – a fairly new culture of this scale. The amnesty programmes, first introduced by the KSA in 2020 and again, recently paved the way on encouraging tax compliance for businesses. The UAE also introduced their amnesty programme this year with the same intention. Perhaps, this could be a temporary solution to gear the economy back on track post pandemic. On whether it will be the norm, is yet to be seen in the next coming years.

What the future will bring

An old-fashioned system was put in place, yet one that has proven its use in revenue collection. It also worked, given the substantial revenues gained from VAT.

The GCC did not opted to immediately adopt more modern, electronic systems as these exist elsewhere (e.g. since a long time in Brazil, but also China).

However, it was identified that E-invoicing was the way to go in the medium run. This is again trodding down a proven path. As often in the GCC, the UAE and KSA show the way. KSA has made E-invoicing mandatory. The UAE and Bahrain have already suggested they will do the same very soon.

No GCC countries have yet announced they will adopt real-time reporting. KSA may be the closest to a potential adoption, given that once phase 2 enters into force in 2023, ZATCA, the KSA tax authority will have access to substantial transactional data. It will allow it to pre-fill the VAT return, and potentially even in real time calculate the VAT.

We’ll see what the future will bring, and for sure in another five years matters will have evolved again drastically, given the pace of changes in the region.

Safe to say that the next 5 years will be equally exciting.

With the publication of an e-Commerce guide and a well established practice since the introduction of VAT on 1 January 2018, this webinar looks at the different aspects of VAT applicable on aspects of e-Commerce. We will give practical examples and show how to comply in practice with the rules. Given the enormous importance of the e-Commerce in the region, this webinar is a must attend for all tax practitioners.

The UAE introduced VAT with effect from 1 January 2018. It based its legislation on the GCC VAT Treaty, which is based on the EU VAT directive, and loosely on a few other jurisdictions. The rules were established in 2017. These were untouched until recently.

For the first time in 2.5 years after the introduction of VAT, the United Arab Emirates (‘UAE’) updated its legislation. The UAE’s Federal Tax Authority (‘FTA’) published an updated version of the VAT Executive Regulations (‘ER’) to the VAT Federal Decree-Law.

The updated version incorporates the changes as per a new Cabinet Decision No. 46 of 2020 (Official Gazette issue 680 of 2020 published on 15 June 2020). The updated version amends one article (article 31 (2)) and improves the English translation in a number of places (e.g., article 51 (5) and article 70 (4). It has flagged only the amendment and not the improvements to the translation. According to the UAE constitution, the amendments enter into effect one month after publication.

This article discusses the change, compares it with KSA and the EU, and analyses the practical complexities and formalities.

Restricting the scope of zero rated exported services

The UAE Federal Cabinet decided to amend one single, but important word. It changed “or” into “and”. The amendment was made to the conditions for considering a recipient “outside of the State”. That condition is necessary in order to consider the services “exported” and therefore zero rated. The amendment highlighted by the FTA was made under Article 31 (2).

For the purpose of paragraph (a) of Clause (1) of this Article, before the amendment the law said, a Person shall be considered as being “outside the State” if they only have a short-term presence in the State of less than a month, or the only presence they have in the State is not effectively connected with the supply.

Now, after the change in law, for the purpose of paragraph (a) of Clause 1 of this Article, a Person shall be considered as being “outside the State” if they only have a short-term presence in the State of less than a month and the presence is not effectively connected with the supply.

Article 31 (2) and (3) of the UAE VAT ER were inspired by the New Zealand GST Act. This can be rather ascribed to a coincidence than a conscious policy choice. Conceptually the NZ GST Act is very different from the GCC VAT Treaty, which is based on the European Union VAT directive (in the UK sometimes informally referred to as the “Principal VAT Directive”).

The NZ’s GST Act also says for the same provision “or”, like in the original text of the UAE VAT ER (see Article 11 A 3 of the NZ GST Act). Note that the examples given by the NZ tax authority for the application of the condition under which the zero rate cannot be applied are very simple, showing that the intended reach is not wide (see https://www.ird.govt.nz/gst/charging-gst/zero-rated-supplies, consulted on 9 July 2020).

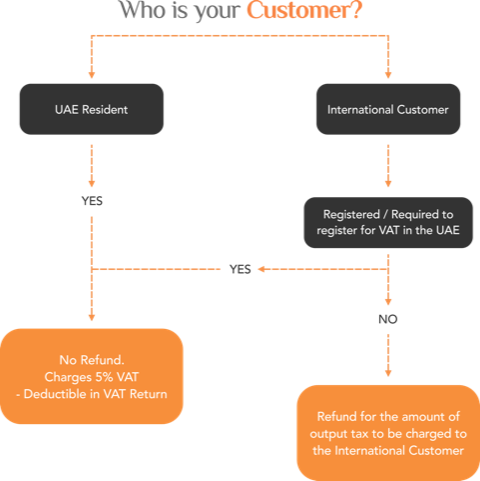

How are services ‘exported’?

To the experienced European VAT adviser the term “exported services” sounds like a badly tuned violin. Yet it is what is referred to as the situation where a service supplier has a customer who is not established in the same country. In that situation, the taxation rights are for the country of the customer, and not the supplier.

In the UAE, this is translated into a long list of requirements. A supply is ‘zero rated’ when the service is supplied to a recipient who does not have a place of residence in an implementing state (GCC countries) and is outside the State at the time the service is performed. Additionally, the service must not be supplied directly in connection with real estate or moveable personal assets situated in the UAE.

Furthermore, services are also subjected to the zero rate in the UAE if they are actually performed outside the implementing states or are the arranging of services that are actually performed outside the implementing states (note that these conflict with the place of supply rules and also overlap with article 54, 1, b of the UAE VAT law). If the supply consists of the facilitation of outbound tour packages, it can also be zero rated.

It is important to note that currently, the UAE does not recognize any of the other GCC countries as an ‘implementing state’. Therefore, ‘outside the State’ also includes customers with a place of residence in other GCC countries.

Comparing zero rates for “exported services”

As a comparison, article 44 of the EU VAT directive simply locates any service rendered to a taxable person abroad in the other country. This place of supply rule is the equivalent of the so-called “export of services”. There is no further restriction to this rule, except to prevent double taxation (article 59a of the EU VAT directive). The “best in class” is therefore very liberal in awarding the ‘zero rate’ to services rendered to a recipient outside of the country of the supplier, when the customer is a taxable person.

Article 45 of the same EU VAT directive locates services which are not rendered to a taxable person in the country of the service supplier (unless amongst others article 59 applies).

The export of services in the UAE applies, irrespective of the status of the customer, whereas in the EU it only applies when dealing with a business customer. If the UAE wanted more revenue, then this was perhaps a place to look for it.

The GCC VAT Treaty prescribes almost the exact same thing as the EU VAT directive and is almost identical in its wording (see articles 15 and 16 of the GCC VAT Treaty, which bear very strong similarities with respectively articles 45 and 44).

The GCC VAT Treaty may however have induced some people in error by using the word ‘taxable customer’ in article 16, which is not a defined term and which should be read equally broad as the term ‘taxable person’ in the Treaty. Note that the GCC VAT Treaty knows no so-called ‘export of services’ and therefore, the rules were likely to be intended to apply as in the EU.

The GCC VAT Treaty does have a cryptic article 34, d, which can actually be considered unnecessary as it solely confirms the rules as they are described above in the Treaty.

KSA has been struggling with the same provision from the GCC VAT Treaty, although it conveniently and surprisingly simply incorporated a Treaty into its domestic laws.

It initially translated article 15 and 16 of the GCC VAT Treaty into article 33 of the Implementing Regulations differently. In July 2019, KSA amended amongst others article 33 to make it more liberal, and closer to the Treaty. KSA wanted to make it less strict to apply the zero rate. Unfortunately though, in practice many businesses in KSA are still very conservative in applying the zero rate, for fear of making a mistake. The VAT rate hike to 15% now puts additional pressure on this conservative position.

Impact of the change – ‘and’ and ‘or’ make a great difference

Since VAT entered into force in January 2018, Article 31 of the UAE VAT ER has been a recurring topic of discussion.

Confusion still reigns in a number of situations to decide whether or not to apply the zero rate to a supply made to a client situated outside the UAE. One notable example is that the service provider may not always know the exact set-up of the client (e.g. does the client have a branch in the UAE?).

By replacing the word ‘or’ with ‘and’ in Article 31 of the UAE VAT ER, the UAE narrowed down the possibilities of considering a customer as being outside the UAE for VAT purposes. This move indicates that the legislator expects more situations where businesses restrict the application of the zero rate on their transactions.

For example, under the new rules, possibly a UAE established and VAT registered service provider will have to refrain from zero rating a supply of services to a foreign client who attends one single meeting in the country, which is connected to the services received.

Vacationing in the UAE is allowed up to 30 days, but the slightest business air that the stay gets, or over staying one day, will make the service provider consider the client as established in the UAE.

The foreign client will then get caught in a situation where it might have to evaluate the extra 5% cost on top of the agreed price for the service.

Even though the UAE has implemented a business refund scheme for non-resident businesses similar to the business VAT refund scheme available in the European Union, the requests take a long time to process, and the approval is not guaranteed.

Additionally, foreign businesses will only be entitled to claim a VAT refund in case they are from a country that has VAT and also provides refunds of VAT to UAE entities in similar circumstances (the so-called reciprocity condition). The refund request is available only for countries that are specified in a list published by the FTA.

This one-word amendment might therefore have far reaching consequences. Service providers who are already cautious to apply the zero rate will stay on the side of caution even more. In a number of cases, i.e. cases where no refund is available to the foreign business, it will simply make doing business 5% more expensive.

The UAE Ministry of Finance denied wanting to increase the VAT rate in the UAE, as KSA did recently when it hiked its standard rate up to 15%. One can imagine the additional cost if it did. The UAE therefore adds itself to a list of countries which favor tax revenue. Adding taxes to ‘exported services’ makes domestic service providers less attractive.

Furthermore, it is also not clear if this change to Article 31(2) intends to prevent the zero rate on supplies made to foreign customers who have a fixed establishment in the UAE (e.g., branch or representative office).

Formally prove your client is outside the State

Perhaps I draw too much from the legislation of the old continent, but it remains the system with the longest experience. In the EU, it suffices that your customer has a foreign VAT number to consider him outside of the state of the service supplier. If the customer is outside the EU, the supplier can use a certificate issued by the client’s tax authority, a VAT number or similar, or any other proof to determine the customer is taxable (Article 18 Council Implementing Regulation No 282/2011 of 15 March 2011).

The UAE’s legislation does not have such criteria, and the tax authority has not stated much in this respect. The supplier is left to his own discretion and will try to collect proof of the establishment of his client abroad. However, there’s only so much one can do. Rechecking the client’s status every time an invoice is issued, may increase the burden on a supplier considerably.

Proving that the conditions for exporting a service are met, is up to the supplier. If the FTA wants to audit these conditions, we may end up in a situation where a supplier needs to give an impossible negative proof, e.g. prove to me that the client did not come to the UAE. How does one do that, other than having the client declare that he did not come. Auditing this point will prove very tricky.

Are you inside the State for the export of services but inside the State for input tax recovery?

The change created ambiguity because the same expression is also defined under Article 52 (2) of the UAE VAT ER. However, this Article was not amended by Cabinet Decision No 46 of 2020.

Article 52 of the UAE VAT ER provides rules for the input VAT recovery in respect of exempt supplies and should be read in conjunction with article 54 (1) (c) of the UAE VAT law, which provides that input tax is recoverable if incurred in respect to supplies that are made outside the State which would have been treated as exempt had they been made within the UAE.

According to Article 52 (2) of the UAE VAT ER, “a Person is outside the State even if they are present in the State, provided it is only a short-term presence in the State of less than a month, or that his presence is not effectively connected with the supply.”

The interpretation of this stand-alone extract could lead one to think that the legislator intended to give businesses a stricter approach to zero-rate a supply while providing a broader understanding when granting input tax credit.

It is not likely that the legislator wanted this, but the truth is that once Cabinet Decision No 46 of 2020 enters into effect, the UAE VAT legislation will have two different understandings of the term “outside the state.”

Small word big change

The small change made to the UAE VAT ER via Cabinet Decision No 46 of 2020, is expected to have a significant impact on resident and non-resident businesses operating in the country.

It added an additional layer of administrative burden on UAE suppliers who now have to prove to the tax authority that their customers are outside the UAE as per the new definition of Article 31 (2) of the UAE VAT ER.

Service providers in the UAE, including consultancy firms and law firms who provide services to non-residents businesses must carefully review their transactions and put in place additional administrative mechanisms to ensure that the zero rate is applied only where the conditions of Article 31 are entirely fulfilled.

Foreign businesses who source services in the UAE must also be aware of the new rules and the risk of incurring 5% extra costs on the services received in case they are not considered as being outside the State at the moment the service is provided.

These businesses need to assess the impact of these amendments on their operations and take the necessary actions to be fully compliant with the new VAT requirements.

The Holy Month of Ramadan is the ninth month of the Islamic calendar, observed by Muslims worldwide as a month of fasting, prayer, self-reflection and enhanced community spirit. The annual observance of Ramadan is one of the five pillars of Islam.

Ramadan is regarded as a time of piety, charity and blessings. Charities and foundations are noticeably more active during the Holy Month, providing assistance to those in need. Meals are provided at mosques, malls and other public places in a spirit of generosity.

Businesses see the Holy Month of Ramadan as an opportunity to organize sales and offer promotions, deals, discounts, gifts and benefits of all kinds. For example, companies may offer “buy one, get one free” or “two for the price of one” promotions or combined offers, where certain products are offered for free or at a reduced priced when bought together with another product (e.g. receiving one year of car insurance free of charge when buying a new car).

Traditionally, businesses also celebrate the Holy month by hosting Iftar parties, hand out Iftar snack boxes or give gifts in cash or in kind during Eid al Fitr, the religious feast which marks the end of Ramadan.

This article discuss how to deal with UAE VAT in the spirit of generosity.

There is no such thing as a free lunch?

VAT does not like free items. It taxes so-called deemed supplies, where businesses give things away for free for which it previously deducted input VAT. However, not all free supplies are deemed supplies. Even though both look similar, i.e. a third party seemingly receives something without paying for it, only deemed supplies carry VAT consequences.

As part of its sales strategy, a business may provide a customer with a free item. A supermarket could offer a ‘buy one get one’ formula, for example for shampoo bottles. Although it is providing the second bottle for free, the customer has actually paid a lower price for two bottles. Therefore, this situation is rather a so-called joint offer, and not a deemed supply.

The same reasoning holds for promotional discounts, where a business is slashing its prices with 50% during Ramadan. A business is not offering half of the product for free, but rather a discount on the price.

Perhaps a business considers giving a different item in addition to the item bought. Upon purchase of an electrical toothbrush, the seller offers 2 free tubes of toothpaste. Although the item is given for free, it is still not a deemed supply. The free item is given with the objective of increasing sales of the main item and is ancillary to it.

It is a very different situation when a grocery store decides to donate food supplies to a shelter or to allow all employees to pick an item from its stock for Ramadan. Those constitute deemed supplies and VAT needs to be charged on them. This means that VAT on these deemed supplies constitutes a cost for the business since it is giving the items for free.

If employers upon purchase however already know that they are purchasing items which are not intended for taxable supplies, they cannot recover the input VAT (and the subject of the deemed supplies is not even on the table).

The business making the deemed supplies needs to issue a tax invoice for the deemed supply and ideally deliver it to the recipient. The VAT on the tax invoice is not deductible in the hands of the recipient.

In the UAE, the taxable value of deemed supplies is its cost. This constitutes the taxable basis on which VAT should be accounted for.

However, even though a supply may constitute a deemed supply, two thresholds apply. If a business stays below the thresholds, it can continue to recover the input VAT and does not have to account for VAT on the deemed supply.

There are two thresholds:

These thresholds allow businesses to occasionally provide small benefits or gifts to their employees and third parties without incurring VAT liabilities.

Given the fact that these thresholds are very low, a business will easily exceed the threshold. Taking into account the substantial administrative burden of having to monitor the thresholds and put a process in place, a business could chose to ignore the thresholds and always account for output VAT. That is also what most informed businesses seem to do.

Entertainment and personal expenses made during Ramadan

VAT is only recoverable when it is paid for goods and services bought for making taxable supplies. However, even though a business may exclusively make taxable supplies, there may still be expenses which are non-recoverable.

When an employer buys items and gives them to its employees for no charge and for their personal benefit, the employer cannot recover the input VAT. For example, if the employer decides to purchase chocolate dates for Ramadan to give to its employees, the input VAT paid is irrecoverable.

The same holds for so-called ‘entertainment expenses’. Entertainment services are “hospitality of any kind”. This includes hotel stays, food and drinks, tickets for shows and events and trips for entertainment.

Therefore, if a business organizes an iftar for its employees and for third parties, the input VAT is not deductible. Even though the event is held with the objective of improving social cohesion and increase sales, and therefore it has a clear business purpose, it is considered an entertainment expense.

In a public clarification published by the Federal Tax Authority, it did confirm however that VAT on certain entertainment costs is recoverable when used for a genuine business purpose, or when incidental to a business purpose. For example, VAT on food and drinks provided during a business meeting, is recoverable, if:

On the other hand, where the hospitality provided becomes an end in itself and is the purpose for attending an event, it will be considered as entertainment costs and VAT is not recoverable.

In other words, if the staff comes for the party or for the Ted talk, the business will not be able to recover the input VAT. If the gathering is serious business, the input VAT will be recoverable.

Complex charities

Despite the fact that charities will mostly carry out transactions which are out of scope of VAT, given they do not charge any consideration, they may still occasionally render taxable supplies and therefore incur certain VAT obligations, such as the obligation to register for VAT purposes.

Charities will mostly receive their income from subsidies or donations. Such income is outside of the scope of VAT. Occasionally, it may provide sponsoring opportunities to business, which are subject to VAT.

Under normal VAT recovery rules, input tax is only recoverable where it relates to taxable supplies. In most cases, charities will therefore be required to allocate and apportion VAT recovery between taxable activities (recoverable) and non-taxable activities or exempt activities (non-recoverable). The input VAT recovery may therefore prove to be quite complex.

A special refund scheme applies to so-called Designated Charities, which meet the criteria set by the Federal Tax Authority.

Conclusion

The Holy Month of Ramadan triggers VAT consequences for businesses. Businesses making sales promotions are required to examine the VAT consequences of these sales promotions. Business also may need to not recover input VAT on certain purchases or charge VAT on a deemed supply when providing employees with entertainment or gifts. Charities also do not have an easy task ahead in calculating their VAT liabilities.

Given the very strict penalty framework, it is important to be aware of the VAT consequences of these activities in order to avoid VAT claims or penalties.

With the influx of more than 25 million visitors expected from around 190 countries for Expo 2020, the UAE FTA has implemented two special VAT refund mechanisms to ensure that business visitors do not incur any VAT.

The first mechanism targets exhibitions and conferences attended by international businesses. The second one benefits business visitors who will be able to claim the refund of VAT paid on expenses incurred in UAE. Below the two mechanisms are discussed.

VAT refund for exhibitions and conferences

The VAT refund for exhibitions and conferences is beneficial for the organizers as well as the business visitors attending such events in the UAE.

This scheme enables both suppliers and their international customers to save 5% VAT payment on selected services. This particular refund mechanism covers services such as the rental of exhibition space or access to exhibitions and conferences.

Only international customers, those who are not established in the UAE or are not registered for VAT purposes in the country, can avail this benefit. The international customer must inform the supplier that the business is not resident in any manner or registered in the UAE for VAT purposes.

The supplier, on the other hand, needs to be registered for VAT purposes in the UAE, as well as inform the FTA before the event takes place to be able to grant this benefit to its international customers.

Once registered, the conference and exhibition supplier should issue an invoice with VAT but not collect VAT on the relevant exhibition or conference services from their customers. Instead, he claims the VAT refund equal to the output VAT charged on the subsequent VAT return.

Since the payment of this VAT will de be deferred to the VAT return and compensated with a simultaneous deduction in the same return, it does not impact the supplier’s cash flow, while also providing the customers with immediate VAT refund.

Refund for business visitors

Similar to the business VAT refund scheme available in the European Union, the UAE has implemented a scheme whereby all VAT costs incurred by a non-resident business which are not registered for VAT in the UAE, are reimbursable through the VAT refund mechanism for business visitors.

Some of the most common expenses by non-residents include the local purchase of goods, employee travel and lodging, training, service charges for vendors and others. It is important to note that the VAT reclaimed must be directly related to the business activities and cannot be for entertainment or any other legally blocked expense, which are specifically excluded from all input VAT recovery.

Foreign business will only be entitled to claim a VAT refund in case they are from a country that has VAT and also provides refunds of VAT to UAE entities in similar circumstances. KSA currently does not provide this refund to UAE businesses. Therefore, the UAE will also not refund businesses from KSA.

The minimum amount of each application for refund of tax is AED 2,000 which may be the amount of single or multiple purchases. The application should be submitted by a calendar year. The FTA will start receiving claims in respect of VAT incurred in 2018 as from April 2019. The opening date for refund applications in subsequent calendar years will be 1st March.

The FTA will soon release further guidance concerning the exact process for claiming the VAT refund. However, it is expected that businesses will have to provide the original tax invoices for which they intend to reclaim the VAT as part of the application.

VAT obligations for non-resident business

Conferences and exhibitions generate significant opportunities for businesses to show their products and close some deals.

However, non-resident businesses who intend to sell goods or provide services during a conference or exhibition in the UAE might need to assess their VAT obligations in the country. For non established businesses, the obligation to register for VAT purposes with the FTA arises from the first taxable supply.

Importantly, non-resident businesses making taxable supplies in the UAE are not entitled to the business visitor refund scheme or to benefit from the VAT refund for exhibitions and conferences.

Overall, these guidelines will not only put UAE top of the list for the hosting of conferences and exhibitions, but it also encourages conference and exhibitions providers, as well as international customers to organize and attend such events in the UAE.

JBC4 3802, Cluster N, Jumeirah Lakes Towers, Dubai, UAE.

201, 14th floor, Al Sarab Tower, ADGM Square, Abu Dhabi, U.A.E.

Al Anoud Tower L18, Office 1802 King Fahad Road Riyadh Saudi Arabia

Regus Business Centre, Floor No. 2, D Ring Road, Al Mataar, Al Qadeer District, Doha, Qatar

© Aurifer

Developed By Volga Tigris Digital Marketing Agency