10 things to know about the UAE’s Country by Country Reporting

The UAE is a popular destination for foreign entities to set up their businesses in the Middle East region, amongst others because there is no corporate income tax on the federal level.

In line with international developments around tax transparency, the UAE decided to align its legislative framework with international tax practices by adopting Country by Country Reporting (“CbCR”). The adoption of BEPS Action 13 (introduction of CbCR legislation) is a strong recommendation from the OECD and is part of the wider OECD BEPS action plan and the Inclusive Framework.

Below we list the top 10 things to know for UAE businesses in relation to the new CbCR.

1. What is a Country by Country Report?

The CbCR is a high level report through which multinational groups report relevant financial and tax information, for each tax jurisdiction in which they do business.

2. Who does it apply to?

The reporting is compulsory for multinational groups which are present in at least two tax jurisdictions and which meet the consolidated revenue threshold of AED 3.15 billion (approx. USD 878 million) in one financial year. The subsidiaries of the group need to be linked through common ownership or control.

3. Which entity files the CbCR?

Multinational groups have to establish which entity must submit this report, the i.e. the ultimate parent entity (“UPE”) or a surrogate parent entity (“SPE”). If the tax jurisdiction of the UPE does not have CbCR legislation or does not (automatically) exchange the reports, the tax jurisdiction of the SPE needs to file the CbCR.

The jurisdiction where the CbCR is filed will automatically exchange the information shared in the CbCR with the other tax jurisdictions in which the group is active.

4. If the UAE entity does not file the CbCR, does it have any other obligation?

If the UAE entity is part of a multinational group, it needs to notify the UAE Ministry of Finance of the name of the entity submitting the CbCR and the tax residence of this entity before the last day of the financial reporting year (31 December 2019 for the first year). There is no formal process in place yet for notifying MoF of this.

5. When do we submit the CbCR?

The CbCR regulations came into effect as of 1 January 2019, this means that for the financial year ending 31 December 2019, the CbCR must be submitted at the latest by 31 December 2020, and annually thereafter.

6. What information should we provide?

The CbCR needs to include the amount of revenues, profits (losses) before income tax, income tax paid, income tax payable, declared capital, accrued profits, number of employees, and non-cash or cash-equivalent assets for each country.

7. What will the CbCR be used for?

The CbCR allows tax authorities around the world to automatically exchange information on taxable profits in different tax jurisdictions. The information allows the tax authorities to make a first assessment before highlighting risk jurisdictions in which too little tax is being paid.

Given the current absence of Federal Corporate Income Tax, the UAE authorities will not have a particular interest in the CbCR. Other States however will be interested in what the UAE subsidiary of the international group is reporting.

8. How long do we keep the information?

The relevant records need to be maintained until 5 years after submitting the CbCR. The records can be kept electronically and in English.

9. Is there a format for submitting the CbCR?

The report should be in the same format as per the OECD guidelines. Click here for Appendix C of OECD’s guide for reference.

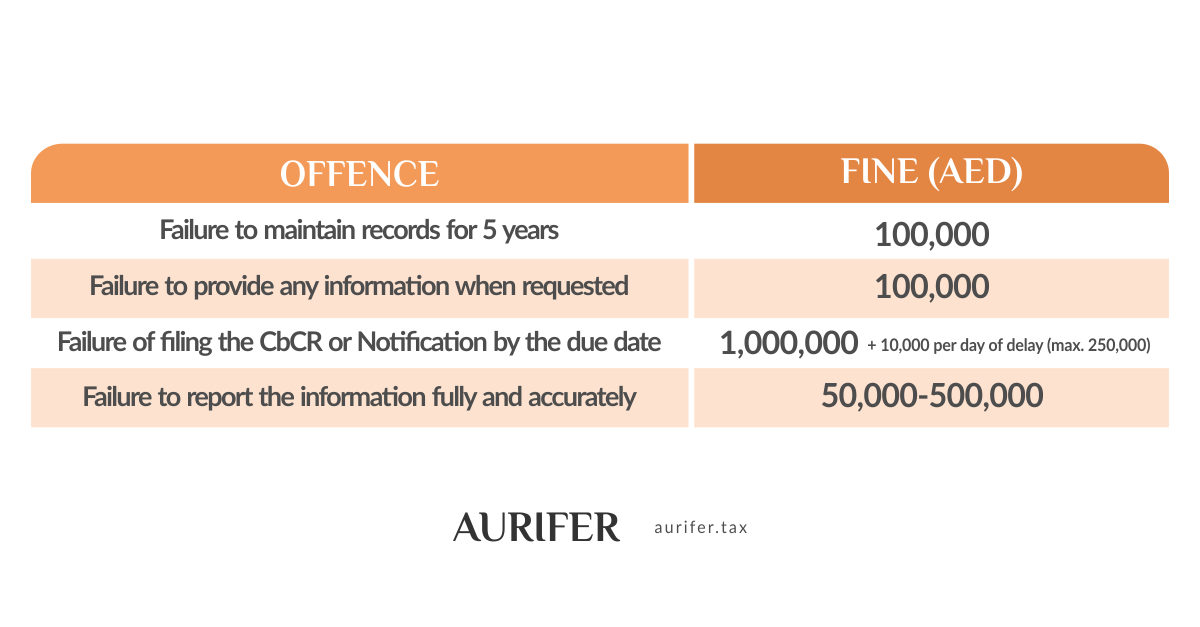

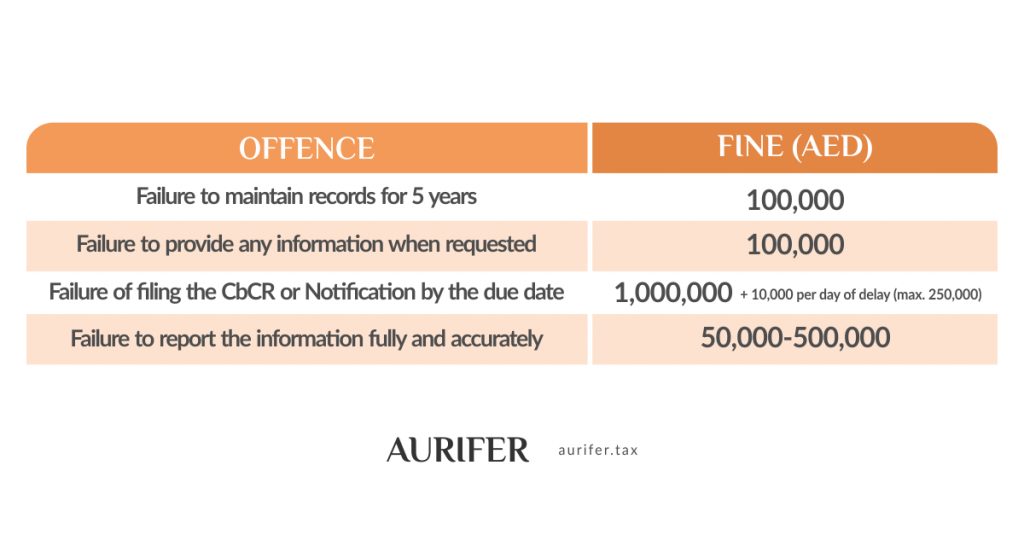

10. Are there any penalties for non-compliance?

(See above table)

Except for the additional daily penalty, the total fines imposed may not exceed AED 1,000,000 in one financial year.