Introduction

On 31 January 2022, the Ministry of Finance (“MoF”) announced that the United Arab Emirates (“UAE”) will introduce a federal Corporate Income Tax (“CIT”) on business profits that will be effective for financial years starting on or after 01 June 2023. This was followed by the release of a Public Consultation Document (“PCD”) in April of 2022 before the publication of the CIT legislation on 9 December 2022.

One of the key elements addressed in the PCD and CIT legislation is with respect to the UAE’s Free Zone Regime. The UAE Free Zone Regime is a system of economic zones established in the UAE that offer favourable conditions for doing business. The Free Zones offer a range of benefits, including 100% foreign ownership, certain tax incentives (including 0% CIT) and simplified administrative procedures.

Subject to certain conditions (summarised in further detail below), “Qualifying Income” of a Qualifying Free Zone Person (“QFZP”) will remain subject to a 0% tax rate under the CIT law for the remainder of the tax incentive period, as provided for in the applicable legislation of the Free Zone in which the QFZP is registered.

As we approach the introduction of the UAE’s CIT regime, many of the burning questions for businesses operating in the UAE revolve around the UAE Free Zone Regime. In particular, the central theme of many people’s inquiries concerns the definition of “Qualifying Income”, which remains subject to a Cabinet Decision.

Given that Non-Qualifying Income shall be subject to CIT at the standard rate of 9%, it is critically important for businesses to understand this definition to appropriately forecast their future tax liability, distributable reserves and manage shareholders’ expectations regarding post-tax profitability etc.

In addition, there are many other practical considerations which taxpayers will be keen to understand going forward. Below we give a short summary of where we stand as well as our thoughts on a number of the key queries and recommendations for businesses in relation to their Free Zone operations.

Where We Stand

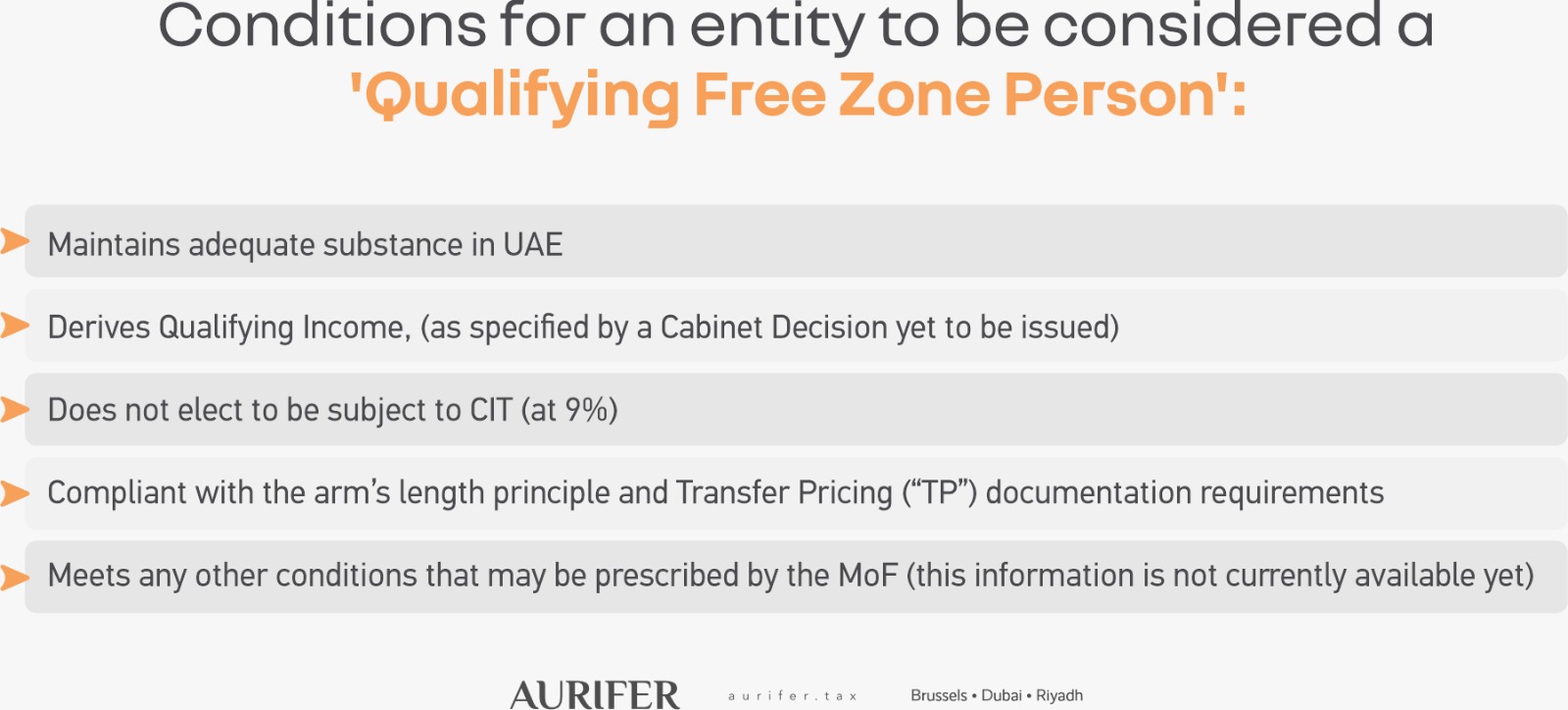

According to Article 18 of UAE CT legislation, an entity operating in a Free Zone is considered a QFZP where it meets all of the following conditions:

Where all these conditions are met, a QFZP shall be subject to zero percent CIT on its Qualifying Income while being subject to tax at 9% on its non-Qualifying Income. Another condition, although not expressly provided in CIT legislation but based on Ministerial Decision No. 73 issued on 6 April 2023, is that a QFZP cannot elect for the Small Business Relief under Article 21 of UAE CT legislation, such that the two regimes are fundamentally alternative.

As discussed above, however, the most critical aspect is that a definition of Qualifying Income is not provided in the CIT legislation but remains subject to a Cabinet Decision yet to be published.

Our Thoughts

In the wait for the Cabinet Decision, one can only advance some hypotheses regarding the scope of application of CIT to QFZP. Below we have outlined some initial thoughts and considerations in relation to each of the abovementioned conditions:

Adequate Substance: We expect this condition will be linked to the Economic Substance Regulations (“ESR”) and the specific criteria used therein. This is primarily due to the Federal Tax Authority’s (“FTA”) familiarity with this approach. Moreover, many Free Zone Persons are already subject to ESR reporting requirements, so it should not cause a major additional administrative burden for the tax administration or the taxpayers. Finally, the lexicon used in the ESR reporting requirements (i.e., “Relevant Activity” and “Core Income Generating Activity”) may suggest a possible analogy between the two pieces of legislation.

Free Zone Persons that do not currently file ESR reports should familiarise themselves with the content and structure in order to best prepare for the future substance requirements.

While we expect that the substance requirement will be linked to the ESR, at the same time, one of the comments that was made by the MoF in its UAE CT Awareness Sessions was that they have so far not decided on whether the ESR regime itself will continue after the CT regime is implemented. More details on this aspect will be issued by the MoF.

Qualifying Income: As outlined above, the definition of Qualifying Income remains the most controversial issue for most businesses operating in the UAE or looking at this geographical area to expand their activities. .Although it is not definitive, the expectation is that the scope of Qualifying Income under the UAE CIT legislation will be broadly in line with the PCD.

In this regard, it is worth noting that while the PCD did not include the terms Qualifying or non-Qualifying Income, it did outline certain types of income earned by Free Zone entities that will be subject to zero percent UAE CIT. We have summarized these below:

Currently, it is assumed that the above income streams would constitute Qualifying Income. However, this ultimately remains subject to the anticipated Cabinet Decision. Being a critical issue for many businesses, we expect specifications in this regard to be disclosed imminently.

Although the PCD remains our best point of reference for Qualifying Income, we note some critical divergences between the PCD and the CIT legislation. For example, reference to both Qualifying and non-Qualifying Income in the CIT legislation suggests partial qualification is available, whereas the PCD implied an “all or nothing” approach whereby any amount of other UAE-mainland sourced income would disqualify a Free Zone Person from the 0% rate in respect of all their income.

While this is a welcome change for businesses with a mix of mainland and foreign-sourced income, it does present some additional practical questions in terms of the calculation of CIT payable on the Non-Qualifying Income of a QFZP. For example:

· Would the AED 375,000 income threshold before applying the 9% CIT rate be charged to the non-Qualifying Income of a QFZP, or would Qualifying Income also be taken into account for the calculation of the AED 375,000 income threshold?

· What is the appropriate method for allocating cost between Qualifying and non-Qualifying Income to determine the final tax liability?

In relation to the first question, it would be prudent at this stage to assume that the income threshold would not apply to non-Qualifying Income of a QFZP. This is supported by the fact that the tax rates applicable for QFZPs are defined in a separate section of Article 3 of the CIT legislation. However, this should become clearer upon issuance of the Cabinet Decision.

With respect to the second question, this should be determined through a combination of appropriate management accounting, transfer pricing policies (for intercompany transactions) as well as preparation of adequate documentation to support the allocation in the event of future audits. In this regard, we expect this to be an area that the FTA will scrutinize due to the potential for manipulation and ultimate reduction of tax payable.

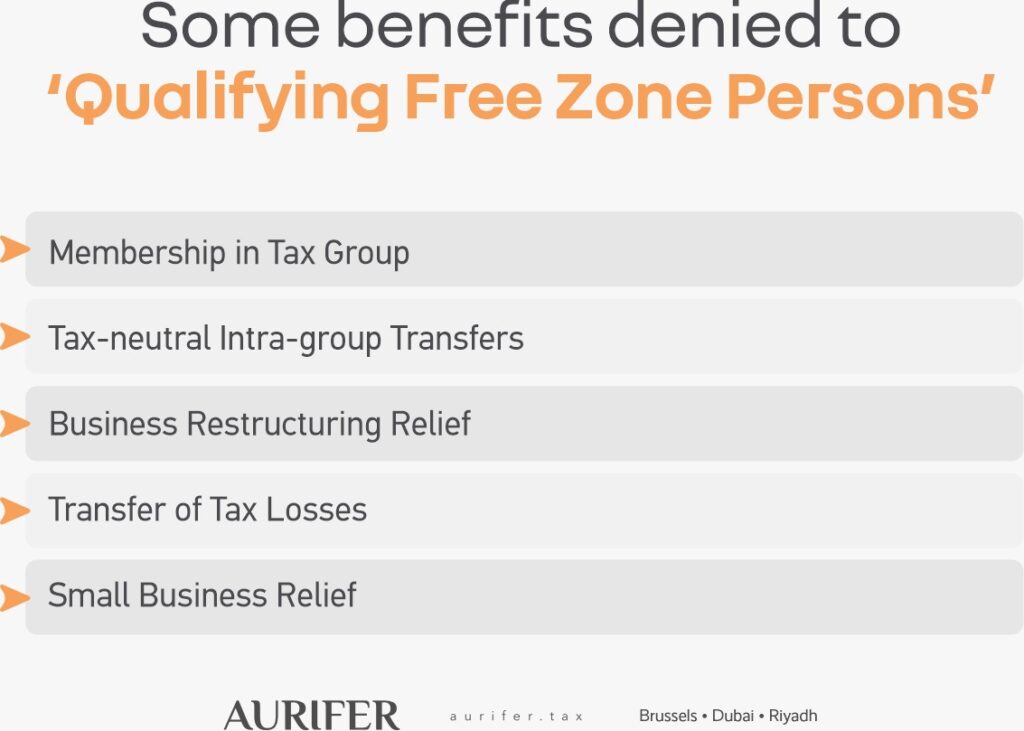

Election for 9%: Under the CIT legislation, QZFPs have the option to ‘elect’ to be subject to tax at the 9% standard rate. Many readers may question why anyone would elect out of such a beneficial regime, if available to them. In this regard, notwithstanding the obvious benefit of the 0% rate there are some restrictions associated with being a QFZP.

For instance, a QFZP cannot become a member of a tax group, it cannot transfer losses to related parties or offset losses from related parties where those related parties are subject to the standard 9% rate. Furthermore, some of the benefits associated with the Free Zone Regime may be largely diminished for multi-national groups that are within scope of Pillar Two. This is discussed in further detail below.

In spite of the above, we expect the Free Zone regime to remain attractive to the large majority of taxpayers. However, our recommendation would be for businesses to perform a holistic assessment of their UAE operations to determine whether the election may be convenient for them once the Cabinet Decision is made public. This should include an assessment of the group’s entire presence in the UAE as well as a cost-benefit or financial modelling exercise to understand whether there is sufficient value in availing of the Free Zone regime.

Transfer Pricing: As part of introducing CIT legislation, the UAE shall also adopt formal Transfer Pricing (TP) regulations for the first time. TP is predicated on the arm’s length principle, which states that the commercial and financial arrangements between related parties are conducted in a manner that is consistent with arrangements between independent enterprises.

In the event that foreign-sourced related party income meets the definition of Qualifying Income, there will be additional scrutiny on payments made to QFZPs going forward from the counter-party jurisdiction. The requirement for transactions to meet the arm’s length principle aligns with the UAE’s commitment to transparency and alignment with international best practices. Additionally, it is important to note domestic transactions are also in scope of TP. As such, Free Zone entities that only transact domestically would still be required to meet this obligation.

The CIT legislation also includes a requirement for taxpayers to prepare adequate TP documentation to support the arm’s length nature of their related party transactions. The UAE’s TP documentation requirements include three components. These components are summarised in the table below:

Businesses should be pro-active in determining an appropriate operating model and transfer pricing policy for their Free Zone operations, including a policy for their transfer pricing documentation.

Other Conditions: Currently, we are not aware of any other conditions that will be announced by the MoF. We expect that this section was included to allow the MoF and FTA some flexibility to make an assessment on whether the current criteria are fit for purpose following the introduction of CIT in the UAE. For example, additional conditions may regard the need to counter abusive arrangements, such as the artificial separation of companies or activity lines to obtain illegitimate tax benefits.

As such, businesses should remain vigilant and attentive to future announcements to ensure they remain fully compliant and can continue using the tax incentives available under the Free Zone Regime.

Pillar Two

The BEPS Pillar Two proposal aims to introduce a global minimum tax rate of fifteen percent on multinationals with annual consolidated revenue above EUR 750m (AED 3.15b). The proposal is designed to ensure that multinational companies pay a fair share of tax wherever they operate, and to prevent them from artificially shifting profits to low-tax jurisdictions.

There are prescribed rules issued by the OECD to calculate a group’s Effective Tax Rate (“ETR”) on a jurisdictional basis to determine the appropriate level of top-up tax required.

Additionally, there are prescribed charging mechanisms to collect any top-up tax payable. These include:

Although the UAE has not announced much in relation to its intentions regarding Pillar Two, many countries and jurisdictions have confirmed they will implement the rules by January 2024 (EU, Switzerland, the UK, South Korea etc.). However, notable nations that have not made any announcements in relation to Pillar Two include the US, India, and Saudi Arabia. We have captured in one of our earlier pieces on the steps available for GCC countries as the world gradually moves towards Pillar Two.

Notwithstanding this, given the wide range of charging mechanisms noted above combined with the ever-growing number of jurisdictions that have announced they will implement, it is clear that the impact of Pillar Two will permeate through to the UAE regardless.

For qualifying multinationals with a QFZP, the benefit of the zero percent rate will likely be reduced through the ETR calculation and subsequent top-up tax payable. However, there may be some reprieve for entities with significant substance in the UAE due to certain measures the OECD has included as part of the Pillar Two model rules which promote substance, such as the Substance Based Income Exclusion and the Routine Profits Test Safe Harbour.

Multinationals should stay alert for future updates from the MoF and the FTA on the UAE’s intentions with Pillar Two and the possible impact on their Free Zone arrangements.

Conclusion

As outlined above, there remains a lot of uncertainty in relation to the UAE Free Zone Regime and how it will interact with the wider introduction of CIT in the UAE. However, it is clear that the Free Zone Regime shall remain a staple of the UAE economy and in most instances will provide a significant tax benefit to entities which qualify as a QFZP. As such, taxpayers should continue to remain attentive and prepare for the journey ahead.