51 years after the inception of the UAE today is the historic day on which the UAE announces the introduction of corporate income tax.

In a historic moment, the Ministry of Finance has announced today that the UAE will introduce a Federal Corporate Income Tax on business profits.

The CIT regime has been implemented by the UAE in view of achieving the following objectives:

We include hereafter the main features of the new regime, as announced by the Mistry of Finance (“MoF”) and the Federal Tax Authority (“FTA”).

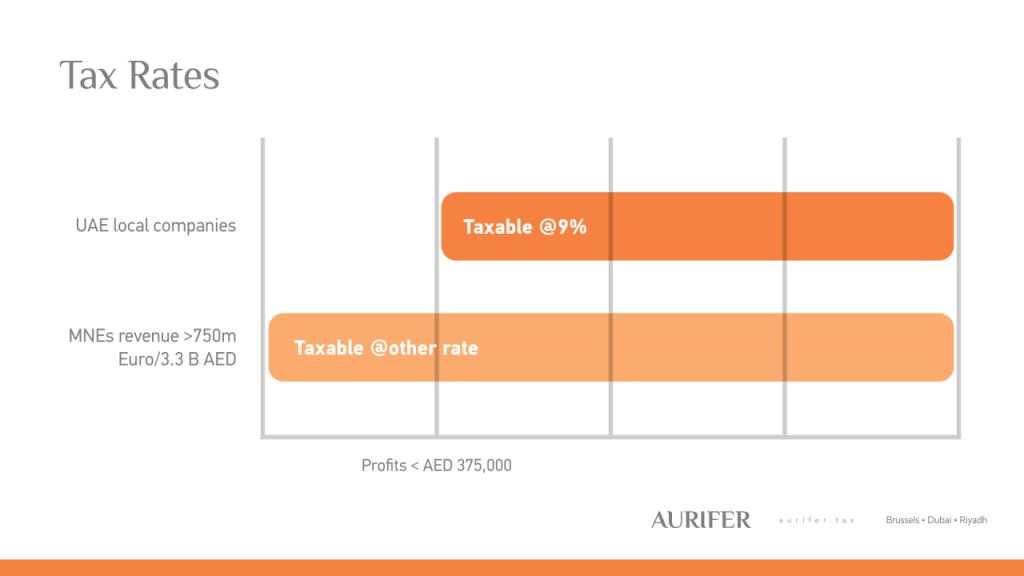

CIT will apply on the worldwide adjusted accounting net profits of the business. The UAE CIT regime introduces three different rates:

For Free zone businesses, the CIT will apply but the tax holidays will continue to be granted to businesses established within UAE free zones that (1) comply with all regulatory requirements and (2) do not conduct business with the UAE mainland. Further details on the compliance obligations of free zone businesses will be provided in due course.

There will be no withholding tax on domestic and cross border payments. This means that foreign investors who do not carry on business in the UAE will in principle not be subject to corporate tax.

In principle, banking operations will be subject to CIT. Further details on the current Emirate level corporate taxation will be provided in due course.

The UAE CIT regime will become effective for financial years starting on or after 1 June 2023. Businesses will become subject to UAE corporate tax from the beginning of their first financial year that starts on or after 1st June 2023.

The following categories of income will not be subject to CIT:

Businesses engaged in real estate management, construction, development, agency and brokerage activities will be subject to UAE CIT.

UAE businesses will need to comply with transfer pricing rules and documentation requirements set with reference to the OECD Transfer Pricing Guidelines. This likely means three tiers, master file, local file and country by country reporting.

The introduction of CIT is a direct result of OECD’s ‘Pillar Two’ which is part of the Base Erosion and Profit Shifting (“BEPS”) project.

With a headline rate of 9% on taxable income, carve outs for start-ups and small business and free zone companies, while at the same time imposing different tax rates for MNEs, the UAE is striking the right balance.

Interesting as well is that with the implementation of CIT, the UAE seems to have also introduced mandatory transfer pricing regulations.

Free zone companies are seemingly outside the scope of the new CIT regime, however, it seems that the carve out is at least subject to certain conditions, such as complying with all regulatory requirements and not conducting business in mainland UAE.

We also anticipate that the implementation of CIT will have an impact on the Economic Substance Regulations that were implemented in 2018.

UAE businesses will need to assess how CIT will apply to their activities and ensure they are ready for the implementation of CIT in 2023. Businesses and tax professionals will have to await the publication of the CIT law to know the exact scope.

For example, the law foresees in an income exemption for dividends received by UAE businesses from qualifying shareholding. What constitutes a qualifying shareholding will depend on the conditions in the law.

We have listed 10 items to be looking out for once the Corporate Income Tax law is published:

© Aurifer

Developed By Volga Tigris Digital Marketing Agency